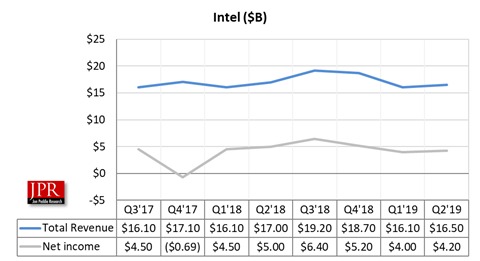

Revenue for the quarter was up 2.5% from last quarter to $16.51 billion, GAAP profit was $4.2 billion, up 5% from last quarter.

Intel reported its calendar Q2 2019; revenues were down year-over-year 3% but grew quarter-to-quarter. Intel achieved 1% growth in the PC-centric business while data-centric revenue declined 7%.

Intel reported its calendar Q2 2019; revenues were down year-over-year 3% but grew quarter-to-quarter. Intel achieved 1% growth in the PC-centric business while data-centric revenue declined 7%.

“Second quarter results exceeded our expectations on both revenue and earnings, as the growth of data and compute-intensive applications are driving customer demand for higher performance products in both our PC-centric and data-centric businesses,” said Bob Swan, Intel CEO. “Based on our outperformance in the quarter, we’re raising our full-year guidance. Intel’s ambitions are as big as ever, our collection of assets is unrivaled, and our transformation continues.”

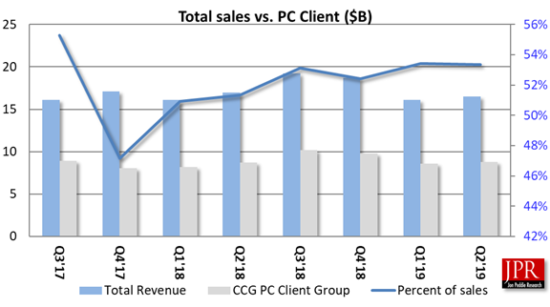

The PC-centric business (CCG) was up 1% in the second quarter due to a strong mix of Intel’s higher performance products, strength in the commercial segment, and customers buying ahead of possible tariff impacts. New, 10-nm-based 10th Gen Intel Core processors (code-named “Ice Lake”) are now shipping and expected to be in volume systems on retail shelves this 2019 holiday selling season.

Collectively, Intel’s data-centric businesses declined 7% YoY in the second quarter. In the Data Center Group (DCG), the communications service provider segment grew 3% while the cloud segment declined 1% and enterprise and government revenue declined 31%. The Internet of Things Group (IOTG) achieved record revenue, up 12% YoY (23% excluding Wind River1) on broad strength and increased demand for higher performance processors. Mobileye achieved second-quarter revenue of $201 million, up 16% YoY on continued customer momentum. Intel’s memory business (NSG) was down 13% YoY in a challenging pricing environment. Intel’s Programmable Solutions Group (PSG) revenue was down 5% YoY in the second quarter.

Spending for R&D was $3.4 billion, up -3% from last quarter, and up 2% from last year.

Client Computing Group

The PC-centric business (CCG) was up 1% in the second quarter due to a strong mix of Intel’s higher performance products, strength in the commercial segment, and customers buying ahead of possible tariff impacts. New, 10-nm-based 10th Gen Intel Core processors (code-named “Ice Lake”) are now shipping, and expected to be in volume systems on retail shelves this 2019 holiday selling season.

In the second quarter, Intel achieved 1% growth in the PC-centric business while data-centric revenue declined 7%.

Just over half (53.3%) of Intel’s revenue comes from client computing. CCG includes platforms designed for end-user form factors, focusing on higher growth segments of 2-in-1, thin-and-light, commercial and gaming, and growing adjacencies such as WiFi and Thunderbolt.

Outlook

The company has raised its full-year revenue outlook to $69.5 billion, up $500 million from April guidance. It is now expecting full-year GAAP EPS of $4.10 and raising full-year non-GAAP EPS outlook to $4.40.

What do we think?

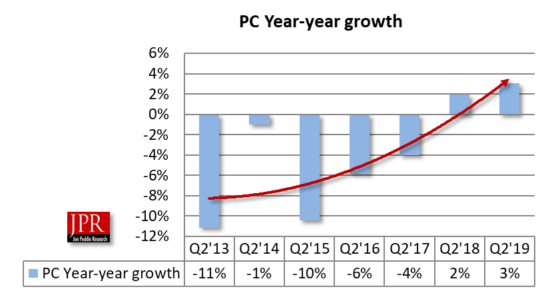

The PC trend has definitely swung up, as shown in figure 4. Having PC sales go up in Q2 is unprecedented and destroys all the seasonality models. However, it may be warp due to pent up demand and Intel’s problems getting its 10 nm parts out in volume.

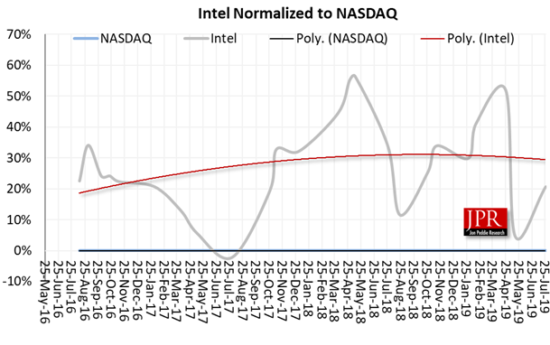

Intel’s share price has returned to the value it was at last year, and increased relative to the NASDAQ.

And, even though Intel bills itself as a data center company, over 50% of overall business comes from the PC, and only 30% from the data center.