Company reports increased ARR and promises continued growth.

Following up on successful Autodesk University and building on its successful transition to subscription presented its investors with a positive accounting of its fiscal quarter Q3, 2019, which ended October 31, 2018. In addition, the company announced its plans to expand its focus on building and construction for the AEC sector with the acquisition of PlanGrid.

Autodesk has declared the transition to subscription successful and this quarter the company reported their ARR (annualized recurring revenue) at $2.53 billion; the company’s subscription plan ARR is at $1.93, an increase of over 108% compared to the same period last year. Finally, total subscriptions are at 4.08 million by the end of the quarter, a 143,000 increase over the previous quarter. In addition to the steady growth of subscriptions.

Because Autodesk has long had subscriptions and maintenance plans, the company distinguishes the current plans from the older plans by calling them subscription plan subscriptions. It might be more accurate to call the current plans rental plans or leases. Never mind, subscription plan subscriptions have increased 252,000 from the previous quarter and are now at 3.12 million, which includes 71,000 maintenance subscribers who have converted to the new product subscriptions. The company puts their deferred revenue at $1.79 billion, almost flat year over year, but combining deferred revenue and unbilled deferred revenue brings the company to $2.24 billion, an increase of 17% year over year. The point is, money is coming in, and there’s more on the way.

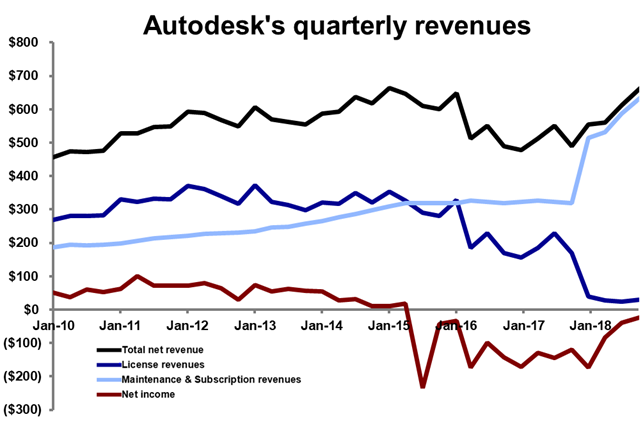

It all adds up to $661 in revenue for the quarter, which is a 28% increase compared to the same period last year.

The company reported a loss of $23.7 million for the quarter. The company has gradually been moving their income up and headed for the black.

Perhaps the most telling statement made in this quarter’s financial call came when CFO Scott Herren told investors that getting their subscriptions above 4 million represents a significant milestone because 4 million “is nearly twice the number of maintenance seats we had at the peak of the previous model.”

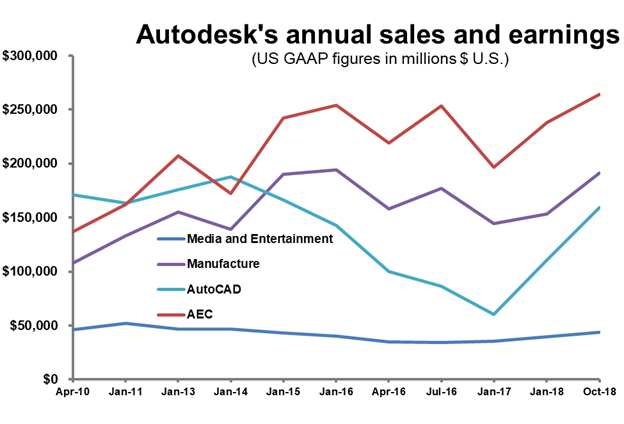

Given the quarter’s results, the company’s faith in AEC is not misplaced. The company says growth was driven by subscriptions for BIM 360. CFO Scott Herren said that of the 143,000 new subscriptions for the quarter, 53,000 of them were for cloud-based services and those subscriptions were led by BIM 360.

Overall subscription plan subscriptions have “more than doubled,” said Anagnost and that’s a continuing trend that has held for seven of the last eight quarters.

During the financial call, CEO Andrew Anagnost talked quite a bit about the PlanGrid acquisition because he sees it as a driver for growth and also a bridge as Autodesk expands the business into the cloud and SaaS. PlanGrid is designed for the construction phase of AEC and is a tool for the workers in the field.

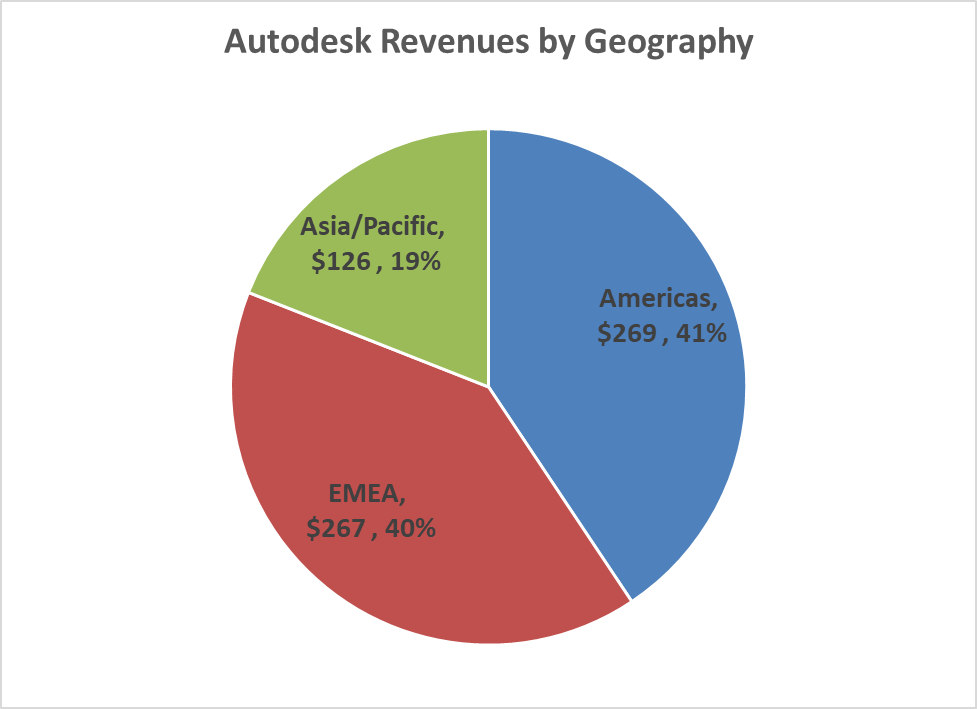

A typical trend that’s evident as software companies transition to subscription models, at least so far, is that the west tends to transition first and the course moves east. At least this is what is being seen for companies based in the U.S. It’s probably a mistake to make too many assumptions about this. It can even be a bit of a self-fulfilling assumption since companies may roll out the changes from their home countries out. For years now, the Americas and EMEA have been very close in revenue for Autodesk, but the attitudes in different countries are very different.

Scott Herren told investors that Autodesk has seen the same patterns for new technologies as well as new business models. He said, “North America seems to be the earliest adopters followed by Continental Europe and then some of the emerging markets in Europe and then APAC comes along. There are different attitudes about what customers expect in terms of service and how they prefer to deal with vendors.” Anagnost noted, for instance, that Japan had been a difficult market for Autodesk but the company did some work with personnel and they’re seeing improvement.

One point to note is that Autodesk has aggressively been trying to convert is maintenance subscription customers to subscription via its M2S program which tinkers with prices for maintenance and AutoCAD LT, making the move to subscription plan subscriptions more attractive. The strategy pays off notes Herren because there is a trend for some conversions to move to more expensive plans. He said of the quarter, “once again, over 30% of eligible subscriptions upgraded from an individual product to an industry collection.”

So, one reason U.S. growth might be a tad lower is that Autodesk is making more progress converting maintenance to subscription plans and therefore there are decreasing eligible subscribers.

What do we think?

Clearly, the subscription model makes sense for enterprise software but what’s really fascinating about Autodesk’s progress through this transition and for the design & produce industry, in general, is how the nature of the industry has changed as well. It’s not really a software business anymore and it’s not even a product market. It’s a systems business. Autodesk, at one time, seemed the most vulnerable at a time of change because of its dependence on AutoCAD as its flagship product. As it has tried various approaches to diversification, the company has evolved into a systems supplier.