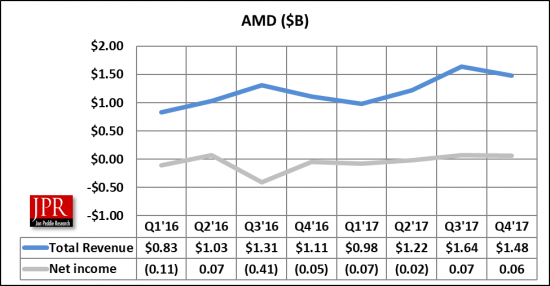

$1.5 billion in sales, $71 million GAAP profit for the quarter, sales and profit down from last quarter.

AMD reported its calendar Q4 2017; revenues and operating income were up as well as its graphics and compute groups revenue and profits.

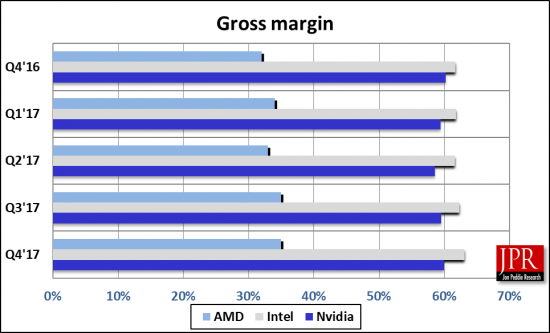

The company’s gross margin was 35%, up 3 percentage points Y/Y, and flat Q/Q.

AMD showed a profit of $301 million for the entire year. Operating income was $82 million, compared to an operating loss of $3 million a year ago and operating income of $126 million in the prior quarter. Net income was $61 million, compared to a net loss of $51 million a year ago and net income of $71 million in the prior quarter.

R&D expenses were $300 million (or 20% of revenue), up $36 million Y/Y and down $15 million Q/Q. SG&A expenses were $133 million (or 9% of revenue), up $12 million Y/Y and up $1 million Q/Q.

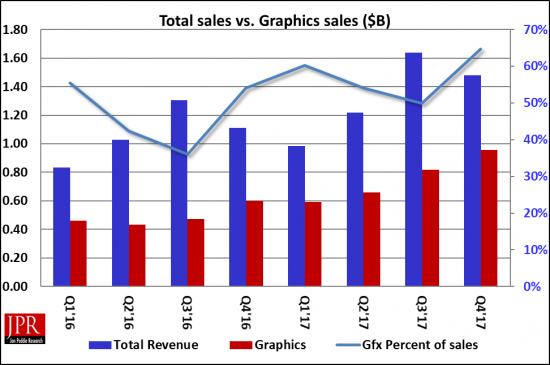

Graphics group

Computing and Graphics segment revenue was $958 million, up 60% Y/Y and 17% Q/Q. The Y/Y and Q/Q increase was primarily driven by strong sales of Radeon graphics and Ryzen desktop processors.

Client average selling price (ASP) increased Y/Y due to an increase in desktop processor ASP, driven by sales of Ryzen processors. Client ASP was flat Q/Q.

GPU ASP increased Y/Y and Q/Q driven by desktop and professional graphics processors ASP.

Operating income was $85 million, compared to an operating loss of $21 million a year ago and operating income of $70 million in the prior quarter. The Y/Y and Q/Q increase was primarily driven by higher revenue.

AMD expanded its presence in the datacenter with new AMD EPYC processor-powered solutions and deployments:

- Microsoft Azure became the first global cloud provider to deploy AMD EPYC processors in its datacenters for its latest L-Series of Virtual Machines.

- Baidu deployed AMD EPYC single-socket platforms to power its AI, big data, and cloud computing datacenters.

- New high-performance platforms powered by AMD EPYC CPUs are now available from ecosystem partners including ASUS, GIGABYTE Technology, and Supermicro.

- The AMD EPYC processor-powered HPE ProLiant DL385 Gen10 server started shipping in volume in December 2017, which launched with record-setting SPEC CPU performance and features leadership cost per virtual machine configurations.

AMD has also launched its Ryzen Mobile Processors with Radeon Vega graphics, which fills out the company’s product line. The company says its AMD Ryzen 7 2700U processor is the world’s fastest processor for ultrathin notebooks. More important, it confirms Su’s statement since introduction of Zen that AMD can produce a full chip lineup on time and according to plan.

- Combining the power of the “Zen” CPU and “Vega” GPU architectures, AMD says Ryzen mobile processors deliver up to 3× the CPU performance, up to 2.3× the GPU performance, and up to 58% less power consumption compared to the previous generation AMD notebook processors.

- Ryzen mobile-based notebooks are currently available from Acer, HP, and Lenovo, with more systems expected from Dell and other OEMs in Q1 2018.

- AMD and Qualcomm announced a collaboration to bring PC connectivity based on Qualcomm Snapdragon LTE modem solutions to high-performance AMD Ryzen mobile processors designed for consumer and enterprise notebooks.

At CES 2018, AMD announced details for upcoming computing and graphics products including its first 7 nm product, a Radeon “Vega” GPU specifically built for machine learning applications, as well as next-generation Ryzen CPUs and desktop Ryzen APUs.

Other

AMD didn’t show the results in the data center that some investors expected. Revenue was $5.33 billion, up 25% from 2016. Enterprise, Embedded and Semi-Custom segment revenue was approximately flat. Gross margin was 34%, up 11 percentage points primarily due to the absence of a $340 million charge recorded in 2016 associated with an amendment to AMD’s wafer supply agreement with GlobalFoundries.

Operating income was $19 million, compared to $47 million a year ago and $84 million in the prior quarter. The Y/Y decrease was primarily due to the absence of a $31 million licensing gain in Q4 2016, and by an increase in R&D expenses, partially offset by the benefit of a richer product mix. The Q/Q decrease was primarily due to seasonally lower semi-custom SoC revenue.

AMD expects revenue to be approximately $1.55 billion for the first quarter of 2018, give or take $50 million. The company is predicting an increase of 32% year-over-year, Ryzen, GPU, and EPYC products ramp over the year.

AMD says in its report: guidance for Q1 2018 and the year-over-year comparison are under the new revenue recognition accounting standard (ASC 606). AMD is adopting the new revenue recognition standard by applying the “full retrospective” method. For comparative purposes under the new standard, Q1 2017 restated revenue was $1.18 billion and Q4 2017 restated revenue was $1.34 billion.

What do we think?

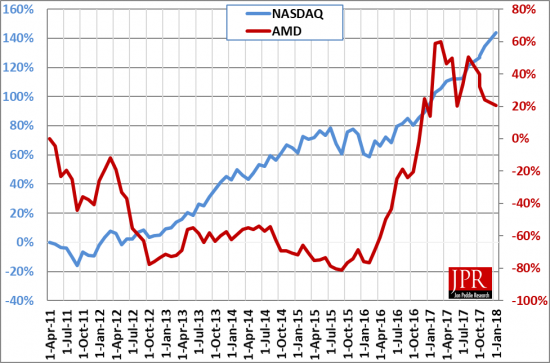

AMD has demonstrated that it has compelling products, is gaining new design wins, and its diversification seems to be delivering strong results. Those are facts. What are not facts are the odds investors place on future performance, based on tea leaves or a lunch with someone who knows someone at AMD. And so, when the company doesn’t meet those expectations it gets sold off and the share price drops.

So the stock market does what the stock market does, but in general doesn’t have any impact on a company’s operation (although it could influence an existing or potential employee’s decision to stay or join, and could impact the company’s ability to raise capital).

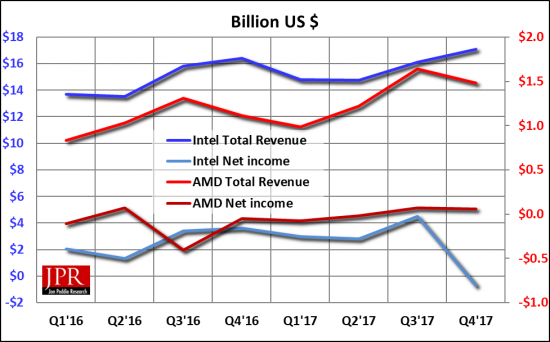

A better yardstick is to compare the company to the industry and its peers. AMD has two and we only have a report from one of them, Intel.

The company has raised its gross margin, which was driving by the Computing and Graphics segment, and was partially due to demand from crypto currency mining issues.

AMD continues to underprice their products and will suffer weak margins until they price closer to their competition.

Their share price will continue to be battered until the company shows some gains in margin. The company’s own CFO has said, “if you’re products are so good, why isn’t your margin higher?”

AMD has to believe in itself and charge a fair market price.