Transition metrics and revenue metrics offer alternative scenarios for Autodesk’s fiscal year.

![]() The story of fourth quarter and full-year results for Autodesk (ADSK: Nasdaq) is a tale of two methods of measurement. If we measure the metrics of transition from perpetual license sales to annual subscriptions, Autodesk is doing quite well. If we measure the more traditional metrics of revenue and income, then fiscal 2016 (ended January 31, 2016) was dull.

The story of fourth quarter and full-year results for Autodesk (ADSK: Nasdaq) is a tale of two methods of measurement. If we measure the metrics of transition from perpetual license sales to annual subscriptions, Autodesk is doing quite well. If we measure the more traditional metrics of revenue and income, then fiscal 2016 (ended January 31, 2016) was dull.

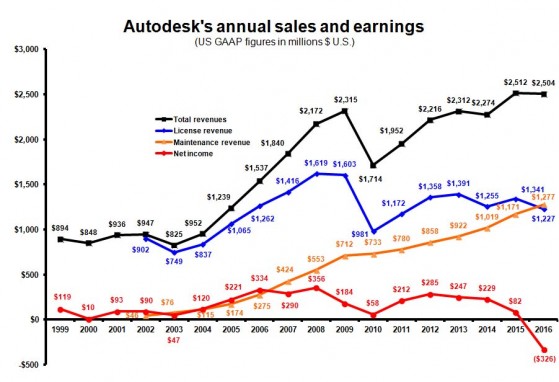

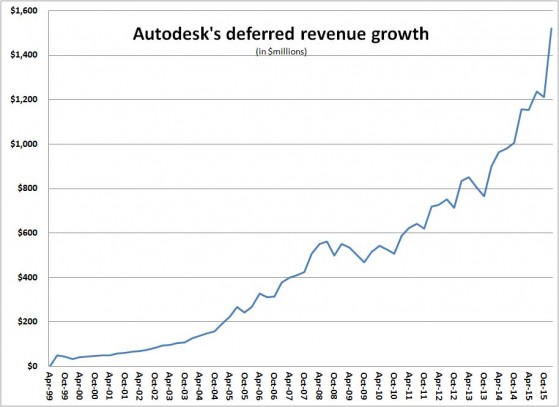

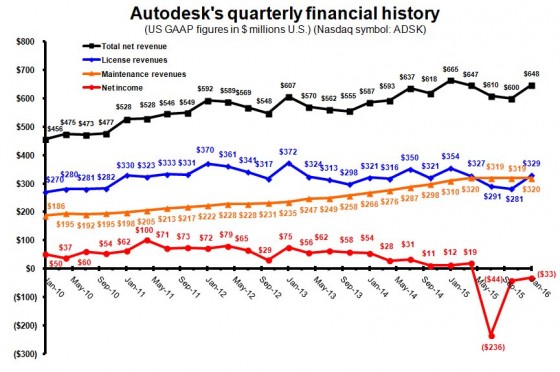

For the fourth quarter of fiscal 2016, Autodesk reports revenue of $648 million, down 2% from a year earlier, but up 3% if measured in constant currencies. The company posted a net loss of $32.7 million, compared to net income of $11.5 million a year earlier. A new metric Autodesk reports, total annualized recurring revenue (ARR) stood at $1.38 billion, up 10% compared to a year ago. Total deferred revenue increased 31% to $1.52 billion, and total billings were up 15% year-over-year.

For all of fiscal 2016 revenue was $2.50 billion, essentially flat compared to FY2015 and up 4% in constant currencies. For the year Autodesk posted a net loss of $326 million, compared to net income of $81.8 million in FY2015.

Of the two ways to measure the company’s results, CEO Carl Bass chose the optimistic route transition metrics. “We had a terrific fourth quarter and our results demonstrate that our business model transition is working. Broad-based demand also led to better than expected subscription additions in the fourth quarter with new model offerings representing well over half of the subscriptions.”

A quote from the company’s announcement seeks to paint a more realistic scenario: “Autodesk is undergoing a business model transition in which the company will discontinue selling new perpetual licenses in favor of subscriptions and flexible license arrangements. During the transition, billings, revenue, gross margin, operating margin, EPS, deferred revenue, and cash flow from operations will be impacted as more revenue is recognized ratably rather than up front and as new offerings bring a wider variety of price points.”

Total subscriptions were 2.58 million, up approximately 109,000 from the previous quarter. New model subscriptions (Desktop, enterprise flexible license, and cloud subscription) were 427,000, up 62,000 from the third quarter. Maintenance subscriptions stood at 2.15 million, an increase of 47,000 from the third quarter.

Drilling into fourth quarter revenue:

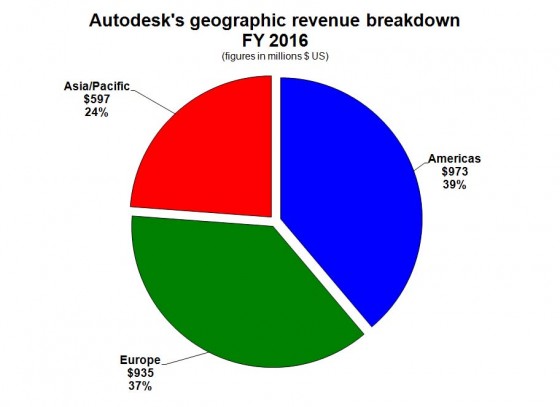

- Americas revenue was $257 million, up 8% from a year ago;

- EMEA revenue was $238 million, down 13% from a year ago and down 4% on a constant currency basis.

- Asia/Pacific revenue was $153 million, down 1% compared 4Q15 and up 6% on a constant currency basis.

- Revenue from emerging economies was $94 million, down 12% from a year ago and down 11% on a constant currency basis. Revenue from emerging economies represented 14% of total revenue in the fourth quarter.

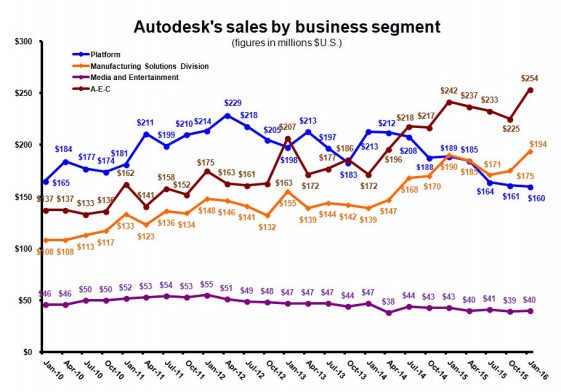

- AEC business segment revenue was $254 million, up 5% from a year ago.

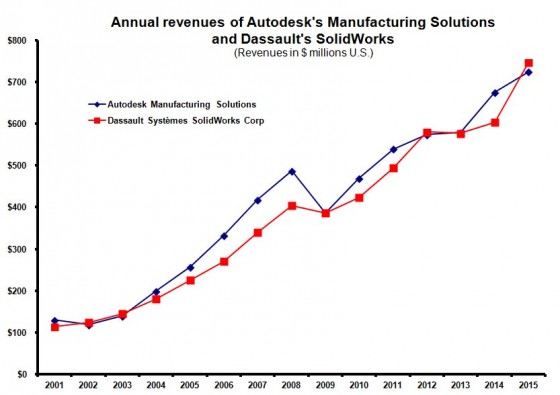

- Manufacturing business segment revenue was $194 million, up 2% compared to the fourth quarter last year.

- Platform Solutions & Emerging Business segment revenue was $160 million, down 15% from 4Q15.

- Media & Entertainment business segment revenue was $40 million, down 7% year-over-year.

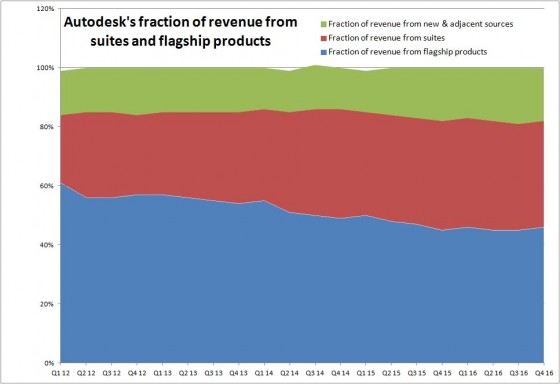

- Flagship products revenue was $296 million, down 1% from a year ago.

- Suites revenue was $232 million, down 7% compared to the fourth quarter last year.

- Revenue from New and Adjacent products was $120 million, up 3% from 4Q15.

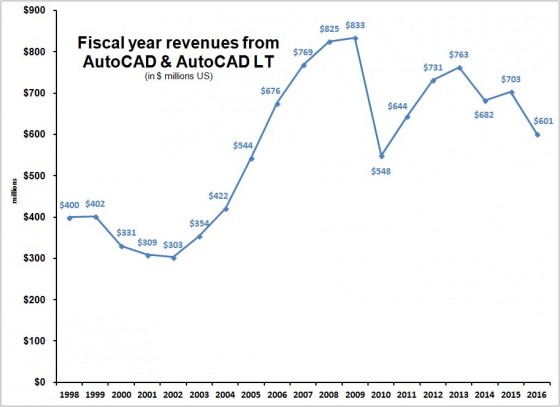

Three more of our custom charts follow.

What do we think?

Usually this is where we put a little extra light on the story. But today is different. L. Stephen Wolfe, P.E., a contributing analyst for Jon Peddie Research, as usual provided research and his usual legendary insights for this article. After more than 30 years as the most respected (by readers) and feared (by vendors) business and technology analyst in the CAD industry, Steve Wolfe is retiring. We wish him well.