GPU shipments decreased -10.3% sequentially and -25% year to year.

Jon Peddie Research reports the growth of the global PC-based graphics processor unit (GPU) market reached 75.5 million units in Q3’22 and PC CPU shipments decreased by -19% year over year. Overall, GPUs will have a compound annual growth rate of 2.8% during 2022–2026 and reach an installed base of 3,138 million units at the end of the forecast period. Over the next five years, the penetration of discrete GPUs (dGPUs) in the PC will grow to reach a level of 26%.

Year-to-year total GPU shipments, which include all platforms and all types of GPUs, decreased by -25.1%, desktop graphics decreased by -15.43%, and notebooks decreased by -30%—the biggest drop since the 2009 recession.

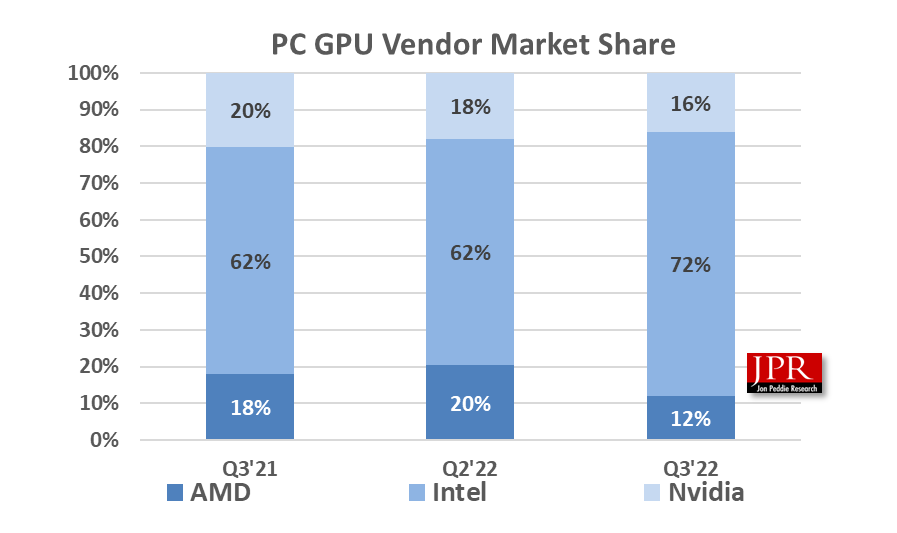

AMD’s overall market share percentage from last quarter decreased by -8.5%, Intel’s market share increased 10.3%, and Nvidia’s market share decreased by -1.87%, as indicated in the following chart.

Overall GPU unit shipments decreased by -10.3% from last quarter, AMD shipments decreased by -47.6%, Intel’s shipments rose 4.7%, and Nvidia’s shipments decreased by -19.7%.

Quick highlights

- The GPU’s overall attach rate (which includes integrated and discrete GPUs, desktop, notebook, and workstations) to PCs for the quarter was 115%, down -6.0% from last quarter.

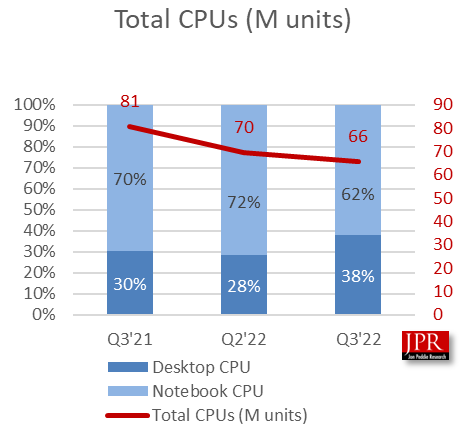

- The overall PC CPU market decreased by -5.7% quarter to quarter and decreased -18.6% year to year.

- Desktop graphics add-in boards (AIBs that use discrete GPUs) decreased by -33.5% from the last quarter.

- This quarter saw 0.5% change in tablet shipments from last quarter.

The third quarter typically has the strongest growth compared to the previous quarter. This quarter was down -10.3% from last quarter, which is below the 10-year average of 5.3%.

GPUs have been a leading indicator of the market because a GPU goes into a system before the suppliers ship the PC. Most of the semiconductor vendors are guiding down for the next quarter, an average of -0.21%. Last quarter they guided -2.79%, which was too high.

Jon Peddie, president of JPR, noted, “The third quarter is usually the high point of the year for the GPU and PC suppliers, and even though the suppliers had guided down in Q2, the results came much below their expectations.

“All the companies gave various and sometimes similar reasons for the downturn. The shutdown of crypto mining, headwinds from China’s zero-tolerance rules and rolling shutdowns, sanctions by the US, user situation from the purchasing run-up during Covid, the Osborne effect on AMD while gamers wait for the new AIBs, inflation and the higher prices of AIBs, overhang inventory run-down, and a bad moon out tonight.”

“Generally, the feeling is Q4 shipments will be down, but ASPs will be up, supply will be fine, and everyone will have a happy holiday,” Peddie said.

JPR also publishes a series of reports on the graphics add-in board market and PC gaming hardware market, which covers the total market, including systems and accessories, and looks at 31 countries.

Pricing and availability

JPR’s Market Watch is available in electronic and hard-copy editions, and sells for $2,750. This report includes an Excel workbook with the data used to create the charts, the charts themselves, and supplemental information. The annual subscription price for JPR’s Market Watch is $5,500 and includes four quarterly issues. Full subscribers to JPR services receive TechWatch (the company’s biweekly report) and a copy of Market Watch as part of their subscription.

Click here to learn more about this significant report or to download it now. For more information, call (415) 435-9368 or visit the Jon Peddie Research website at www.jonpeddie.com.

Contact Robert Dow at JPR ([email protected]) for a free sample of TechWatch.