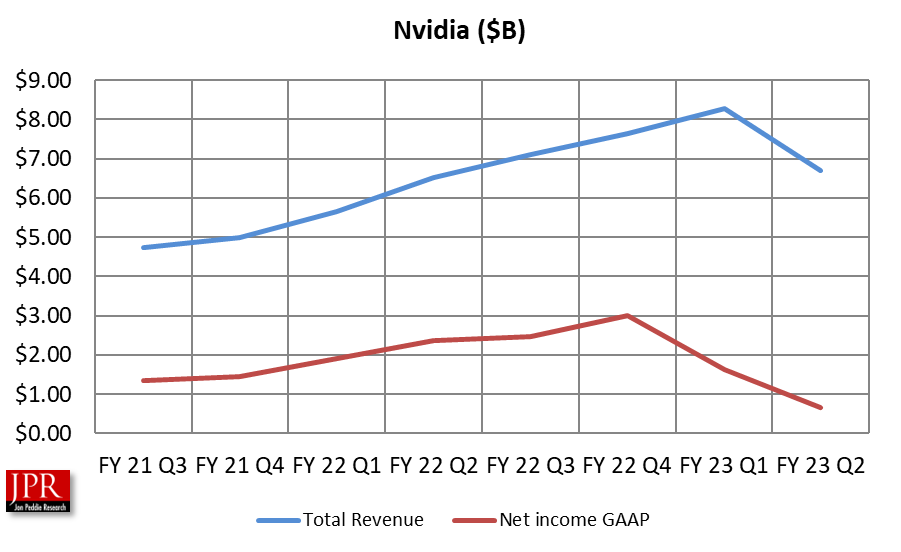

Revenue $6.7 billion, down 19% from last quarter; profit down 59%.

Nvidia reported revenue for the second quarter ending July 31, 2022, of $6.7 billion, up 3% from a year ago and down 19% from the previous quarter.

GAAP earnings per diluted share for the quarter were $0.26, down 72% from a year ago and down 59% from the previous quarter. Non-GAAP earnings per diluted share were $0.51, down 51% from a year ago and down 63% from the previous quarter.

“We are navigating our supply chain transitions in a challenging macro environment, and we will get through this,” said Jensen Huang, founder and CEO of Nvidia. “Accelerated computing and AI, the pioneering work of our company, are transforming industries. Automotive is becoming a tech industry and is on track to be our next billion-dollar business. Advances in AI are driving our Data Center business while accelerating breakthroughs in fields from drug discovery to climate science to robotics.

“I look forward to next month’s GTC conference, where we will share new advances in RTX, as well as breakthroughs in AI and the metaverse, the next evolution of the Internet,” he said.

Nvidia said that during the second quarter of fiscal 2023, it had returned to shareholders $3.44 billion in share repurchases and cash dividends, following a return of $2.10 billion in the first quarter. The company has $11.93 billion remaining under its share repurchase authorization through December 2023. Nvidia plans to continue share repurchases this fiscal year.

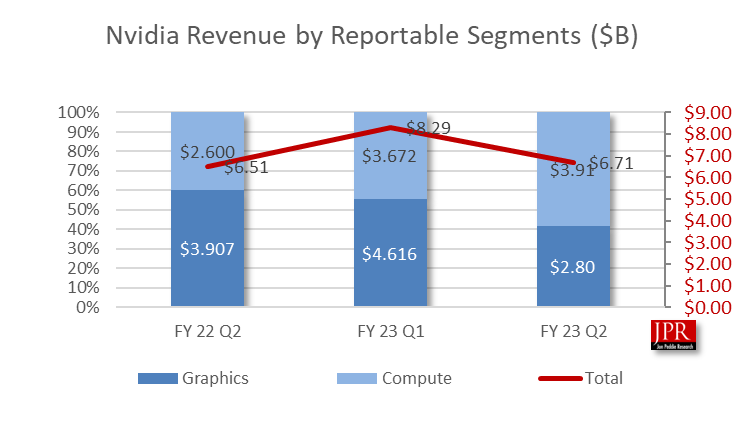

Revenue was lower than the company’s outlook issued in May, primarily due to weaker Gaming revenue, the company said. Data Center revenue was somewhat short of Nvidia’s expectations, as it was impacted by supply chain disruptions, Nvidia added.

Gaming revenue was down 33% from a year ago and down 44% sequentially. These decreases were primarily attributable to lower sell-in of gaming products, reflecting reduced channel partner sales due to macroeconomic headwinds. In addition to reducing sell-in, the company implemented pricing programs with channel partners to address challenging market conditions, which are expected to persist into the third quarter.

Nvidia’s GPUs are capable of cryptocurrency mining, though it has limited visibility into how much this impacts its overall GPU demand. Volatility in the cryptocurrency market—such as declines in cryptocurrency prices or changes in the method of verifying transactions, including proof of work or proof of stake—has in the past impacted, and can in the future impact, demand for its products and the company’s ability to accurately estimate it. As noted last quarter, Nvidia had expected cryptocurrency mining to make a diminishing contribution to gaming demand. According to Nvidia, it is unable to accurately quantify the extent to which reduced cryptocurrency mining contributed to the decline in gaming demand.

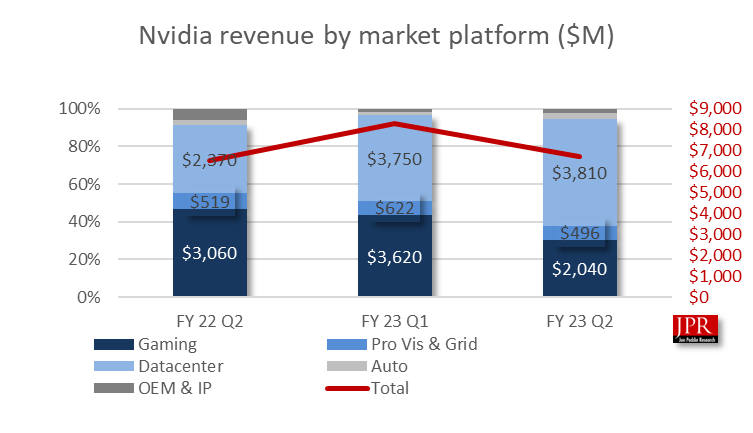

Data Center revenue was up 61% from a year ago and up 1% sequentially. Nvidia said the year-on-year increase was primarily driven by hyperscale customer revenue, which nearly doubled. Sequentially, sales to North America hyperscale and cloud computing customers increased but were more than offset by lower sales to China hyperscale customers affected by economic conditions in China. Vertical industries grew both sequentially and year-on-year. Key workloads driving growth included natural language processing, deep recommenders, autonomous vehicle fleet data processing and training, and cloud graphics.

Professional Visualization revenue was down 4% from a year ago and down 20% sequentially. The sequential increase in mobile revenue was more than offset by lower desktop revenue, particularly at the high end.

Automotive revenue was up 45% from a year ago and up 59% sequentially. These increases were driven by revenue from self-driving and AI cockpit solutions, said the company, partially offset by a decline of legacy cockpit revenue.

OEM and Other revenue was down 66% from a year ago and down 11% sequentially. The sequential decline was driven by lower notebook OEM sales, partially offset by higher Jetson sales, according to Nvidia. Cryptocurrency Mining Processor (CMP) revenue—$266 million a year ago—was nominal in the current and prior quarter.

Data Center revenue included $287 million for orders originally scheduled for delivery primarily in the third quarter that were converted to second-quarter delivery with extended payment terms, while a number of second-quarter orders will be fulfilled in the third quarter given supply chain disruptions.

Third quarter of fiscal 2023 outlook

Nvidia says it has slowed operating expense growth, balancing investments for long-term revenue growth, while managing near-term profitability. The company’s full-year non-GAAP operating expense is expected to grow by over 30%. The outlook for the third quarter of fiscal 2023 is as follows:

- Revenue is expected to be $5.90 billion, plus or minus 2%. Gaming and Professional Visualization revenues are expected to decline sequentially, as OEMs and channel partners reduce inventory levels to align with current levels of demand and prepare for the company’s new product generation. Nvidia expects that decline to be partially offset by sequential growth in Data Center and Automotive.

- GAAP and non-GAAP gross margins are expected to be 62.4% and 65.0%, respectively, plus or minus 50 basis points.

- GAAP and non-GAAP operating expenses are expected to be approximately $2.59 billion and $1.82 billion, respectively.

- GAAP and non-GAAP other income and expense are expected to be an expense of approximately $10 million, excluding gains and losses from non-affiliated investments.

- GAAP and non-GAAP tax rates are expected to be 9.5%, plus or minus 1%, excluding any discrete items.

- Capital expenditures are expected to be approximately $550 million to $600 million, including principal payments on property and equipment.

GAAP and non-GAAP gross margin decreases were primarily due to a $1.34 billion charge, comprising $1.22 billion for inventory and related reserves and $122 million for warranty reserves.

The $1.22 billion charge for inventory and related reserves is based on revised expectations of future demand, primarily relating to Data Center and Gaming. The charge consists of approximately $570 million for inventory on hand and approximately $650 million for inventory purchase obligations in excess of their current demand projections, and cancellation and underutilization penalties.

What do we think?

Nvidia has been an above-average manager of production, inventory, and cash flow; their record speaks for itself. However, this is the second time the company misread the crypto market and got too far ahead in inventory buildup. But, it wasn’t just crypto that left them with too much inventory; desktop gaming, notebook, and workstations were all down significantly across the entire PC market. Supply chain interruptions and delays in China didn’t help matters, nor did inflation, as the company tried to make tactical changes in a volatile market. Semiconductor production and delivery is a long process. It takes over a quarter from placing orders to a fab to delivering product to the channel and OEMs. A lot can go wrong during that process, and this year, a lot of uncontrollable and unforeseeable things did—basically, a planetary disruption. No company in the industry escaped unscathed despite what they might say.

This will iron itself out, and by the end of the year, barring any more surprises from viruses, wars, weather, and politics, things should be running smoothly again. Regardless, Nvidia as always has their eyes on the future and says they are underserving demand in the data center while holding back supply in the channel to let it drain.