Upsetting traditional models, reporting, and forecasts, cryptocurrency-mining has distorted the mechanisms for reporting sales and has driven up pricing for graphics boards.

At Jon Peddie Research, we have been tracking the impact of cryptocurrency-mining on the add-in boards (AIB) market since the beginning of 2017 and have published reports that identify the number of AIBs, used specifically for cryptocurrency-mining and their market value.

The average price of an AIB cryptocurrency-mining since April 2016 has gone up an average of 343% overall. The average ASP for AIBs from Q1’12 to Q4’15 dropped 31%, and then started going up.

Prices of individual AIBs fluctuate for a variety of reasons, but the overall trend has been a lowering of the ASP of AIBs till the mining boom hit.

These price increases are having a boomerang effect, causing some people to postpone buying a new AIB (for gaming, photo-editing, or design work). As a result, the lessened demand could let prices come back down as inventory builds up in the channel. However, for the next couple of quarters we expect seesaw-like activity as price-elasticity effects test the consumer’s and the miner’s resolve.

Inflated AIB prices will increase branded PC sales

What will the run up in AIB prices do to PC pricing? Probably not very much immediately, as the OEMs negotiate their deals six months ahead of shipping a PC and buy direct instead of through the opportunistic distribution channels, which have enthusiastically raised prices. However, smaller white box (WB), custom system integrators (SIs) and VARs who build to order and don’t carry inventory will find they have to raise prices (or give up profit to remain competitive) against the branded PCs. As SI, VAR, and WB vendors raise prices, buyers (usually SMB and Enterprise) customers will shift their orders to the brand names with stable and lower pricing. Price (plus local supply and service, and maybe custom features) are the cornerstone of SIs and VARs. As a result, the price shift will hurt the more vulnerable in the industry and favor the large OEMs—at least temporarily.

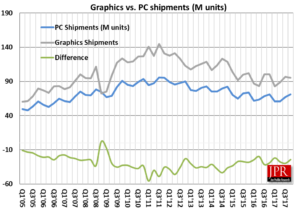

The PC market has not expanded

Since the PC research firms like Gartner, HSI, and IDC estimate the shipments of WB, SI, and VAR suppliers, seeing branded PC sales go up may lead them to a false conclusion about the overall PC industry. This may already have happened. In Q4, PC sales were reported higher from the previous quarter, while AIB sales were down. The processor suppliers did see their shipments go up slightly. However, not all processors go into PCs. The PC research firms try to compensate for SI/VAR/WH shipments with an “Other” category. It is impossible to measure the shipments of those non-branded suppliers, so the research firms use a model, one they’ve honed for decades. One of the major components to it are processor shipments. In Q4’17, we estimate 71.7 million x86 processors were shipped. In that same time period, Gartner estimated 71.6 million PCs shipped (19.6% in other), and IDC estimated 70.6 million PCs (with 17.6% in other).

The problem with keying off processor shipments for PC sales is the latency of the manufacturing process. It takes two to four months from the time AMD or Intel ships an x86 processor until the time a branded PC supplier ships one of their systems with that processor. Therefore, Q3 processor shipments should be more in line with Q4 PC shipments. Shipments of a supplier also depend on how a given company recognizes a sale. Some recognize a sale when ownership transfers to the buyer—when an invoice is issued. However, most of the channel suppliers (Amazon, Alibaba, BestBuy, Tesco, etc.) have contract terms stipulating that after a certain amount of time, if a product hasn’t been sold, it can be returned to the supplier, so channel suppliers don’t recognize products sent to them as a sale to them until they sell it. That is done to minimize accounts payable and inventory, things all companies want to minimize, which gives them a very high reported throughput and low days-of-inventory, all done at the expense of the PC vendor.

All that makes it devilishly difficult, if not impossible to estimate actual PC shipments.

Based on GPU shipments (discrete and integrated), which declined 1.5% in Q4 from Q3, we disagree with the PC research firms that actual PC shipments increased 6% in the same time period and think the PC research firms need to adjust their models, especially in view of the inflated dGPU shipments due to cryptocurrency-mining.

We disagree with the PC research firms that claim actual PC shipments increased 6% in Q4.

It will take a quarter or two for the PC research firms to get their models straightened out and not set their client’s hair on fire, all the while the dGPU cryptocurrency-mining shipments will be fluctuating.

Epilog

Although we contend that the PC market has not expanded as reported, we do think the category of the PC market will expand in 2018, just not based on x86 processors alone. The introduction of Arm-based PCs in the form of always connected PCs will indeed increase PC shipments, where a PC is designated as a device that runs Microsoft windows or other x86 compatible operating systems. The Arm-based PCs will be totally integrated graphics and as such change the attach rate for the PC market. That will cause us (JPR) to change our models too. The good news is the PC market is not static, the bad news is the PC market is not static which makes it damn tough to forecast, and even report on. Wouldn’t have it any other way, it’d be boring otherwise.

Related stories:

Tech Republic comments on Cryptocurrency-mining market effects