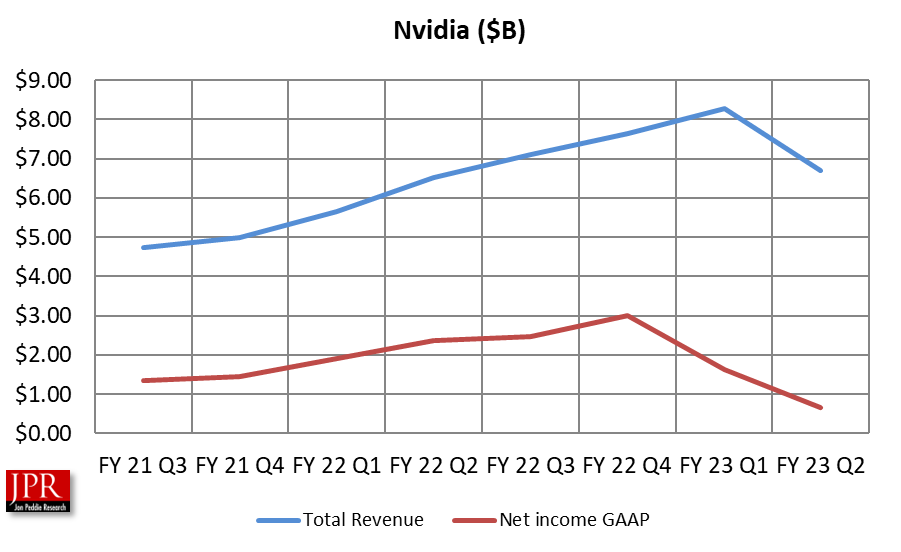

The company reports revenue of $5.93 billion, down 17% from a year ago and down 12% from the previous quarter.

Nvidia reported revenue for its third fiscal quarter ended October 30, 2022, of $5.93 billion, down 17% from a year ago and down 12% from the previous quarter.

GAAP earnings per diluted share for the quarter were $0.27, down 72% from a year ago and up 4% from the previous quarter. Non-GAAP earnings per diluted share were $0.58, down 50% from a year ago and up 14% from the previous quarter.

“We are quickly adapting to the macro environment, correcting inventory levels and paving the way for new products,” said Jensen Huang, founder and CEO of Nvidia. “The ramp of our new platforms—Ada Lovelace RTX graphics, Hopper AI computing, BlueField and Quantum networking, Orin for autonomous vehicles and robotics, and Omniverse—is off to a great start and forms the foundation of our next phase of growth.

“Nvidia’s pioneering work in accelerated computing is more vital than ever. Limited by physics, general-purpose computing has slowed to a crawl, just as AI demands more computing. Accelerated computing lets companies achieve orders-of-magnitude increases in productivity while saving money and the environment,” he said.

During the third quarter of fiscal 2023, Nvidia returned to shareholders $3.75 billion in share repurchases and cash dividends, bringing the return in the first three quarters to $9.29 billion. As of October 30, 2022, the company had $8.28 billion remaining under its share repurchase authorization through December 2023.

Nvidia will pay its next quarterly cash dividend of $0.04 per share on December 22, 2022, to all shareholders of record on December 1, 2022.

Revenue matched projections made last quarter: Nvidia projected revenue of $5.90 billion last August, and it reported $5.93 billion. It also met GAAP operating expense projections of approximately $2.59 billion projected and $2.57 actual. Where it fell short was GAAP gross margins; it projected 62.4% but delivered 53.6%.

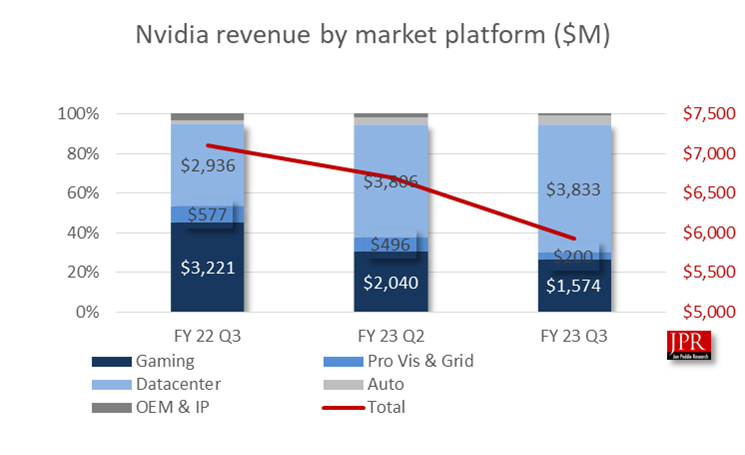

Gaming revenue was down 51% from a year ago and down 23% sequentially. The decline reflects lower sell-in to partners to help align channel inventory levels with current demand expectations as macroeconomic conditions and Covid lockdowns in China continue to weigh on consumer demand.

The year-on-year decrease was driven by lower GPU sales for both desktops and laptops; the sequential decline was primarily driven by lower GPU sales for laptops. The reduced utility of GPUs for crypto mining may have contributed to increased aftermarket sales of GPUs in certain markets.

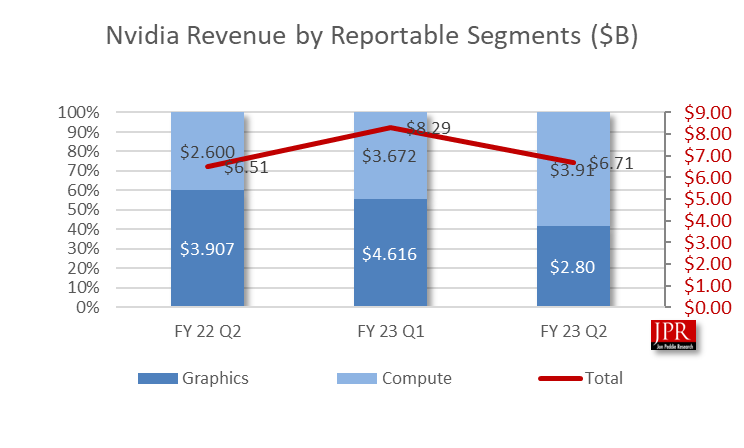

Data Center revenue was up 31% from a year ago and up 1% sequentially. Year-on-year growth was broad-based across US cloud service providers, consumer Internet companies, and other vertical industries. Sequential growth was impacted by softness in China.

Nvidia started shipping its new H100 data center GPU based on the new Hopper architecture during the third quarter. Also in Q3, the US government announced new restrictions on exports of their A100- and H100-based products to China, and any product destined for certain systems or entities in China. These restrictions impacted third-quarter revenue, with the decline largely offset by sales of alternative products into China.

Professional Visualization revenue was down 65% from a year ago and down 60% sequentially, reflecting lower sell-in to partners to help align channel inventory levels with current demand expectations.

Automotive revenue was up 86% from a year ago and up 14% sequentially, primarily driven by revenue from self-driving solutions.

OEM and Other revenue was down 69% from a year ago and down 48% sequentially. The sequential decline was driven by lower Jetson and notebook OEM sales. Cryptocurrency Mining Processor (CMP) revenue was nominal in the current and prior quarter, and $105 million in the third quarter of fiscal 2022.

Fourth quarter of fiscal 2023 outlook

Nvidia says it has slowed operating expense growth, balancing investments for long-term revenue growth, while managing near-term profitability. The company’s full-year non-GAAP operating expense is expected to grow by over 30%.

For the fourth quarter of fiscal 2023, Nvidia expects revenue to be $6.00 billion, plus or minus 2%. GAAP and non-GAAP gross margins are expected to be 63.2% and 66.0%, respectively, plus or minus 50 basis points. GAAP and non-GAAP operating expenses are expected to be approximately $2.56 billion and $1.78 billion, respectively.

GAAP and non-GAAP other income and expense are expected to be an income of approximately $40 million, excluding gains and losses from non-affiliated investments. GAAP and non-GAAP tax rates are expected to be 9.0%, plus or minus 1%, excluding any discrete items.

What do we think?

Nvidia’s guidance for the quarter doesn’t seem to take into account some very positive tailwinds for the company. It has the 40 series of cards coming out with good reviews and a decent supply. The bloom is off the rose on crypto mining, which is seeing a precipitous drop in used pricing (of course, that may be a problem for the 40 series). And it’s the holiday season, with talk of recession easing.

The downside is sales are off in the consumer market due to inflation pressures and the Biden administration has kneecapped China sales. Semiconductor production and delivery is a long process, and it could take more than a quarter to start delivering product to the channel, so it could miss the Christmas window.

Another challenge is managing inventory. Nvidia’s inventory has shot from $2.6 billion in January to $4.45 billion in October. No vendor wants to be stuck with inventory, least of all one with new product coming out.

This will iron itself out and by the end of the year, barring any more surprises from viruses, wars, weather, and politics, things should be running smoothly again. Regardless, Nvidia as always has their eyes on the future and says they are underserving demand in the data center while holding back supply in the channel to let it drain.