Cost reductions and efficiency improvements planned.

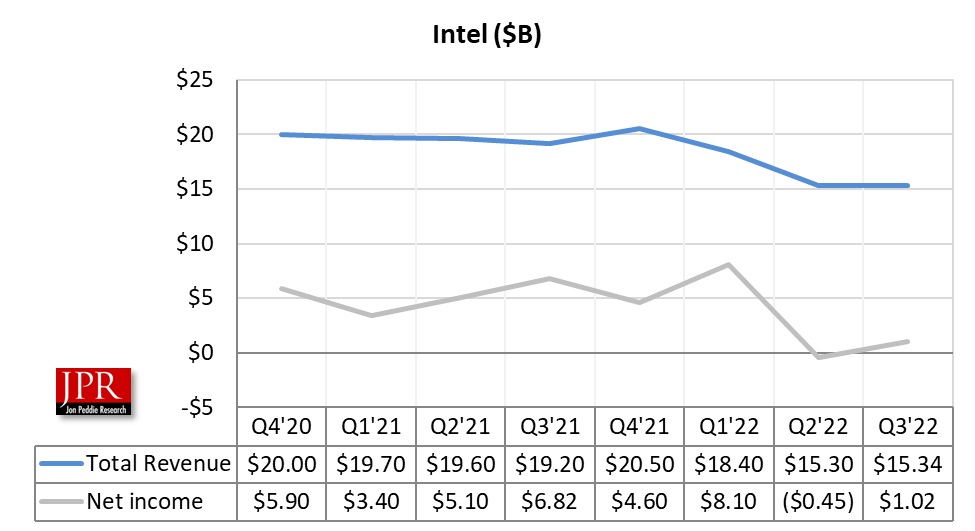

Q3’22 was a tough quarter for all semiconductor companies, including Intel. The company’s Q3 revenue was flat sequentially and modestly below the midpoint of its guidance. In June, Intel was one of the first companies to announce an abrupt and pronounced slowdown in demand, which has broadened beyond initial expectations and is now having an industrywide impact across the electronics supply chain. The company has adjusted its Q4 outlook and is planning for the economic uncertainty to persist into 2023.

Gross margin, once as high as 70%, has dropped to 40%.

“Despite the worsening economic conditions, we delivered solid results and made significant progress with our product and process execution during the quarter,” said Pat Gelsinger, Intel CEO. “To position ourselves for this business cycle, we are aggressively addressing costs and driving efficiencies across the business to accelerate our IDM 2.0 flywheel for the digital future.”

While they are not satisfied with their results, Gelsinger said Intel remains laser-focused on controlling what they can and are pleased that their PC share stabilized in Q2 and is now showing meaningful improvement in Q3.

Intel’s server share, while not where they would like it to be, is (says the company) tracking in line with its expectations and they are encouraged by good execution in the quarter against their product road map. In addition, the company is intensifying its cost-reduction and efficiency efforts, and says they are aggressively moving into the next phase of IDM 2.0, geared to unlocking the full potential of the IDM advantage.

“As we usher in the next phase of IDM 2.0, we are focused on embracing an internal foundry model to allow our manufacturing group and business units to be more agile, make better decisions, and establish a leadership cost structure,” said David Zinsner, Intel CFO. “We remain committed to the strategy and long-term financial model communicated at our Investor Meeting.”

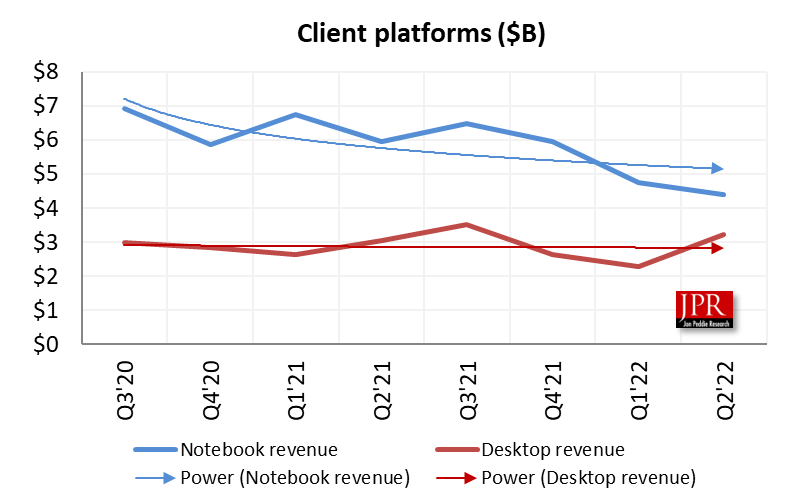

Notebook revenue was $4.4 billion, down $1.5 billion from Q3 2021. Notebook unit sales decreased 28%, driven by lower demand in the consumer and education market segments. Notebook ASPs increased 3% due to an increased mix of commercial products and lower mix of consumer and education products.

Desktop revenue was $3.2 billion, up $103 million from Q3 2021. Desktop unit sales increased 2% partially due to increased demand for enthusiast and gaming products, while ASPs remained flat.

Other revenue was $492 million, down $233 million, primarily driven by the continued ramp-down from the exit of their 5G smartphone modem business and lower demand for their wireless and connectivity products.

In a prepared statement, Gelsinger said would be focusing his comments in three areas:

- The key trends and dynamics that shaped Q3 and are informing their outlook.

- The progress they are making on IDM 2.0, including the company’s momentum on process and product road maps, and their recent announcement that they are implementing an internal foundry model.

- The actions underway to drive cost savings and efficiency gains aimed at accelerating their transformation.

Gelsinger then continued on with his address:

Specific to trends we are seeing, along with further deterioration in consumer PC demand in Q3, enterprise demand has begun to slow. We expect PC units to decline mid-to-high teens to approximately 295 million units in calendar-year 2022. Our own Q3 results reflect a strong product portfolio with Raptor Lake building on Alder Lake’s momentum, as well as working closely with customers to optimize their inventory, our market share, and our business objectives. We are still shipping below PC consumption, and the inventory correction continued in Q3, but not as quickly as we forecasted. Importantly, however, PC usage remains strong, demonstrating the increased utility and value of the PC and, ultimately, supporting a TAM well above pre-pandemic levels. We are targeting a calendar-year 2023 PC unit TAM of between 270 and 295 million units, with a strong brand and product line driving additional share especially at premium ASPs.

The data center TAM is holding up better, although enterprise and China continue to show signs of weakness, as do some, but not all, cloud customers. Across our infrastructure and industrial-exposed businesses, NEX demand was very solid, though not immune from the weakening economy. PSG continues to be a true standout with record Q3 revenue, up over 25% year over year. PSG backlog is robust, and it continues to be an area where we are supply-chain-limited.

Despite the challenging business environment, we made solid progress toward our long-term transformation in Q3, and we remain fully committed to using the macro uncertainty to accelerate our efforts. Each quarter, our confidence grows in achieving our goal of five nodes in four years. On Intel 4, we are progressing towards high-volume manufacturing and will tape-out the production stepping of Meteor Lake in Q4. The first stepping of Granite Rapids is out of the fab, yielding well, with Intel 3 continuing to progress on schedule. Intel 4 and Intel 3 are our first nodes deploying EUV and will represent a major step forward in terms of transistor performance per watt and density. On Intel 20A and Intel 18A, the first nodes to benefit from RibbonFet and PowerVia, our first internal test chips and those of a major potential foundry customer have taped-out with silicon running in the fab. We continue to be on track to regain transistor performance and power performance leadership by 2025.

IFS is a major beneficiary of our TD progress, and we are excited to welcome Nvidia to the RAMP-C program, which enables both commercial foundry customers and the US Department of Defense to take advantage of Intel’s at-scale investments in leading-edge technologies. Since Q2, IFS has expanded engagements to seven out of the 10 largest foundry customers coupled with consistent pipeline growth to include 35 customer test chips. In addition, IFS increased qualified opportunities by $1 billion to over $7 billion in deal value, all before we welcome the Tower team with the expected completion of the merger in Q1 of 2023.

On the product front, we had a busy quarter. Within client, as mentioned earlier, we added to the strong Alder Lake momentum with the launch of Raptor Lake DT in Q3, driving a more than 40% improvement in multithread performance and unquestioned leadership in gaming, with 6 GHz out of the box and record-setting overclocking. We currently have over 500 OEM design wins. We launched Intel Unison to deliver best-in-industry multidevice UX. In addition, we saw meaningful development progress across multiple OEM designs on Intel 4-based Meteor Lake, with volume ramps in 2023. We now have all elements of the AXG portfolio in production, with A770 giving our discrete graphics efforts a strong boost. The Flex family is building a strong pipeline of data center use cases, and Ponte Vecchio is now in production for HPC offerings and production blades deployed for lead customers. Combined with Sapphire Rapids and Sapphire Rapids HBM, Ponte Vecchio is the basis for strong traction with HPC customers like Argonne National Laboratory and Germany’s Leibniz Supercomputing Center.

The rest of Gelsinger’s comments can be found here.

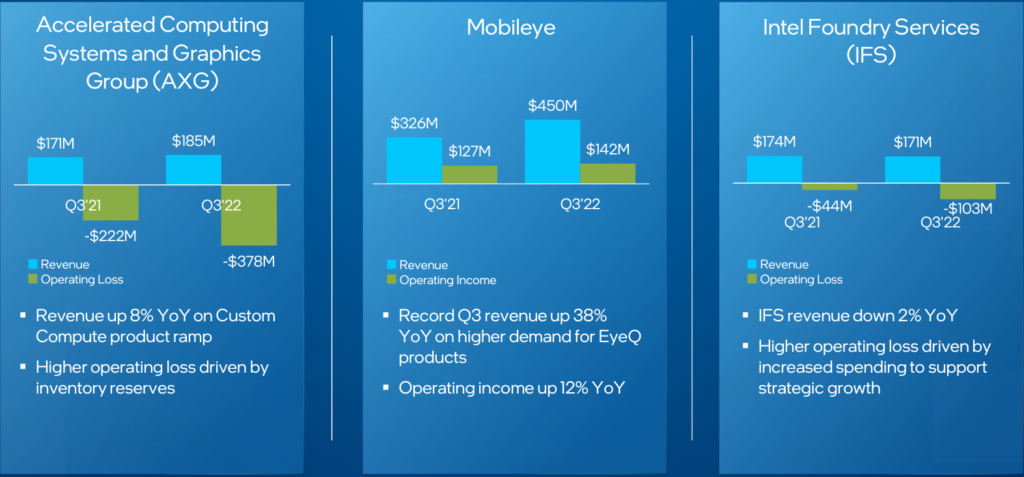

AXG launched the Intel Data Center GPU Flex Series GPU for a wide range of visual cloud workloads, and the Intel Arc A770 and A750 desktop GPUs.

This week, Mobileye went public on the Nasdaq Stock Exchange, which Intel believes will unlock value for Intel’s stockholders.

IFS announced that Nvidia has joined the US Department of Defense’s RAMP-C program.

Outlook

Intel is adjusting its Q4 outlook and is planning for the economic uncertainty to persist into 2023.

The company expects revenue for Q3’22 to be between $14 billion and $15 billion, down 23% to 28% YoY. Gross margin should increase to 45%, up QoQ, down 10.9 ppt YoY. EPS should hit $0.20, down 83% YoY.

What do we think?

The macroeconomic data of the US doesn’t quite agree with the somewhat pessimistic report and forecast of Intel, which indicates issues beyond external economic influences are at work within the company.

Data released from the US Bureau of Economic Analysis shows that the nation’s gross domestic product—the total value of goods and services produced in the US—was up in the third quarter of 2022, increasing at an annual rate of 2.6%. That increase reflected increases in exports, consumer spending, nonresidential fixed investment, federal government spending, and state and local government spending, as well as decreases in imports. That growth was partly offset by lower housing sales.

Disposable personal income and personal savings were also up.

New York Times economic and business reporter Ben Casselman noted the data from the past three quarters—two down, one up—shows that the economy is slowing, and he suggested that this quarter’s big swing upward is due to changes in trade and inventories. But, he pointed out, slowing the economy a bit is exactly what the Federal Reserve is trying to do: slow demand to bring down inflation. No doubt, Intel took this into account in their forecasts.