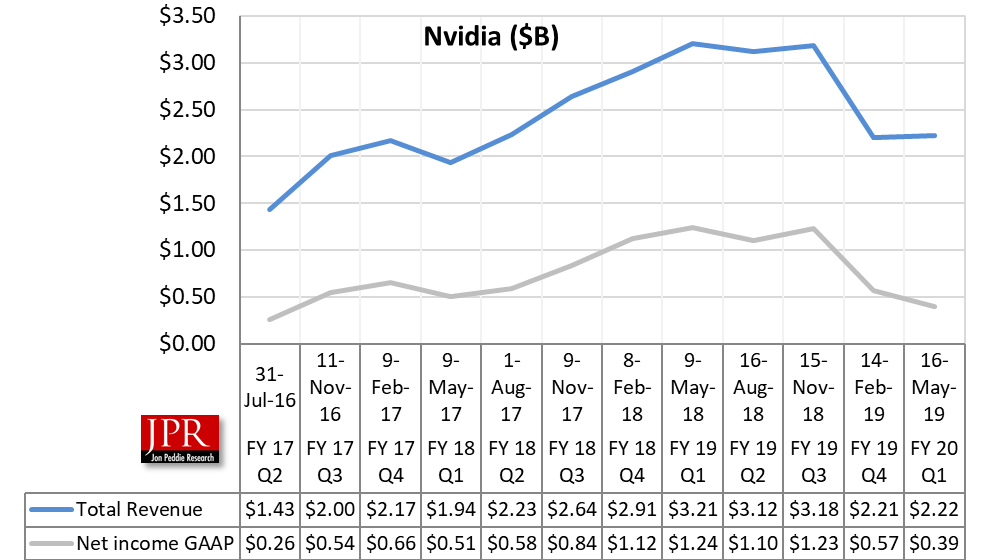

$2.2 billion in sales, $394 million profit; down 31 % from last quarter.

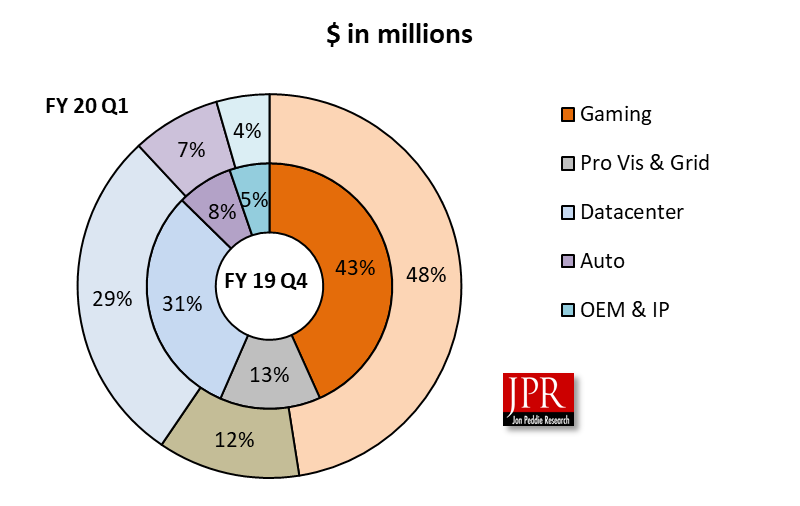

Nvidia reported revenue from some platforms—Gaming and Automotive, the revenue up; while Data center, Professional Visualization, and OEM saw a decline quarter-to-quarter.

The company’s GPU business revenue was $2.02 billion, down 27% from a year earlier and up 2% sequentially.

“NVIDIA is back on an upward trajectory,” said Jensen Huang, founder, and CEO of Nvidia. “We’ve returned to growth in gaming, with nearly 100 new GeForce Max-Q laptops shipping. And Nvidia RTX has gained broad industry support, making ray tracing the standard for next-generation gaming.”

GAAP gross margin decreased to 58.4% for the first quarter of the fiscal year 2020 from 64.5% for the first quarter of the fiscal year 2019. The decrease in the fiscal year 2020 is primarily due to the company’s gaming margins and mix shifts across the portfolio.

GPU business revenue was $2.02 billion, down 27% from the year earlier and up 2% sequentially. The year-on-year decrease reflects declines in gaming and data center revenue, as the company as well as the absence of $289 million of OEM revenue from cryptocurrency mining processors.

Tegra Processor business revenue—which includes automotive, SOC modules for gaming platforms, and embedded edge AI platforms—was $198 million, down 55% from a year ago and down 12% sequentially. The year-on-year decrease primarily reflects a decline in shipments of SOC modules for gaming platforms.

Gaming revenue was $1.05 billion, down 39% from a year ago and up 11% sequentially. The year-on-year decrease primarily reflects a decline in shipments of gaming GPUs and SOC modules for gaming platforms. The sequential increase primarily reflects growth in gaming GPUs. The company believes a shortage of Intel processors that is impacting the global PC market will affect its sales of gaming GPUs for laptops in the second quarter of the fiscal year 2020.

Professional Visualization revenue was $266 million, up 6% from a year earlier and down 9% sequentially. The year-on-year increase, says the company, reflects strength across both desktop and mobile workstation products. The sequential decrease largely reflects a seasonal decline.

Data Center revenue was $634 million, down 10% from a year ago and down 7% sequentially, primarily reflecting a slowdown in purchases by certain hyperscale and enterprise customers, partially offset by growth in inference sales. The company believes this slowdown in purchases will likely persist into the second quarter of the fiscal year 2020.

Automotive revenue of $166 million was up 14% from a year earlier and up 2% sequentially, primarily reflecting growth in AI cockpit modules.

OEM and Other revenue were $99 million, down 74% from a year ago and down 15% sequentially. The year-on-year decrease is primarily due to the absence of $ 289 million from CMP sales.

Capital return to shareholders: The company intends to return $3.0 billion to shareholders by the end of the fiscal year 2020, including $700 million in share repurchases made during the fourth quarter of the fiscal year 2019. In the first quarter of the fiscal year 2020, Nvidia returned $97 million in quarterly cash dividends. Nvidia intends to return the remaining $2.20 billion by the end of the fiscal year 2020, through a combination of share repurchases and cash dividends. As of April 28, 2019, Nvidia was authorized, subject to certain specifications, to repurchase additional shares of our common stock up to $7.24 billion through December 2022.

During the quarter, Nvidia entered into an Agreement and Plan of Merger, with Mellanox Technologies Ltd. Nvidia will acquire all of the issued and outstanding common shares of Mellanox for $125 per share in cash, representing a total enterprise value of approximately $6.9 billion as of the date of the Merger Agreement. The closing of the merger is subject to certain conditions, including the approval by Mellanox shareholders and various regulatory agencies. If the Merger Agreement is terminated under certain circumstances involving the failure to obtain required regulatory approvals, the company could be obligated to pay Mellanox a termination fee of $350 million.

During the first quarter of the fiscal year 2020, the company introduced the GeForce GTX 1660 Ti, GTX 1660 and GTX 1650 gaming GPUs based on Turing GPUs and announced that real-time ray tracing is now integrated into Unreal Engine and Unity commercial game engines.

For professional visualization, the company announced expanded adoption of Nvidia RTX ray-tracing technology by top 3D application providers and unveiled the Nvidia Omniverse open-collaboration platform to simplify creative workflows for content creation.

For its data center platform, the company introduced the Nvidia CUDA-X AI platform for accelerating data science; announced availability of Nvidia T4 Tensor Core GPUs from leading OEMs and Amazon.

Also, during the first quarter of the fiscal year 2020, the company their partnership with Toyota Research Institute Advanced Development to develop, train and validate self-driving vehicles; unveiled the Nvidia Drive AP2X automated driving solution.

Outlook

The company’s outlook for the second quarter of fiscal 2020 is as follows:

- Revenue is expected to be $2.55 billion, plus or minus 2 percent.

- GAAP and non-GAAP gross margins are expected to be 59.2 percent and 59.5 percent, respectively, plus or minus 50 basis points.

- GAAP and non-GAAP operating expenses are expected to be approximately $985 million and $765 million, respectively. The sequential change in GAAP operating expenses reflects an increase in stock-based compensation.

- GAAP and non-GAAP other income and expense are both expected to be an income of approximately $27 million.

- GAAP and non-GAAP tax rates are both expected to be 10 percent, plus or minus 1 percent, excluding any discrete items. GAAP discrete items include excess tax benefits or deficiencies related to stock-based compensation, which are expected to generate variability on a quarter by quarter basis.

- Capital expenditures are expected to be approximately $120 million to $140 million For fiscal 2020, revenue is expected to be flat to down slightly.

What do we think?

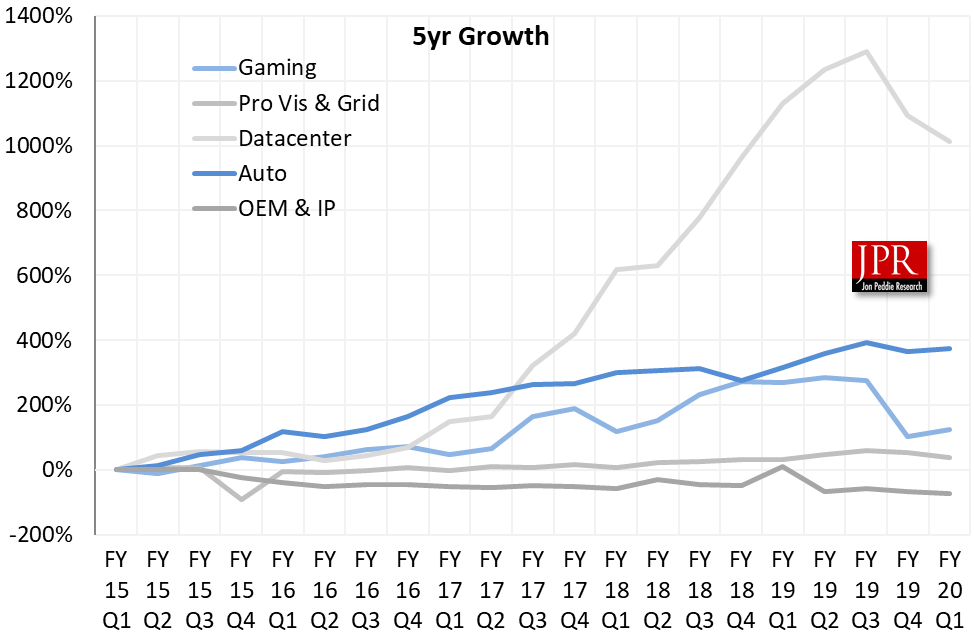

Once again, Gaming buoyed Nvidia’s sales enough to overcome the declines in Data Center and Pro-Viz. Automotive made a slight contribution in the quarter in segment sales but declined in the percentage of overall sales.

Tegra sales were down 55% from a year ago and down 12% sequentially, primarily reflecting a decline in shipments of SOC modules for gaming platforms—i.e., Nintendo’s Switch sales.

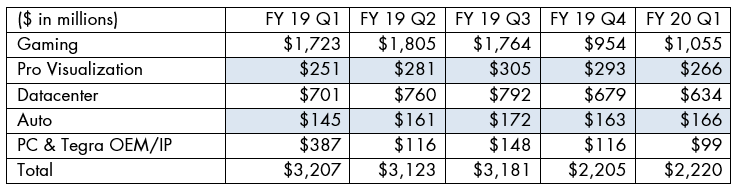

The numeric values are shown in the following table.

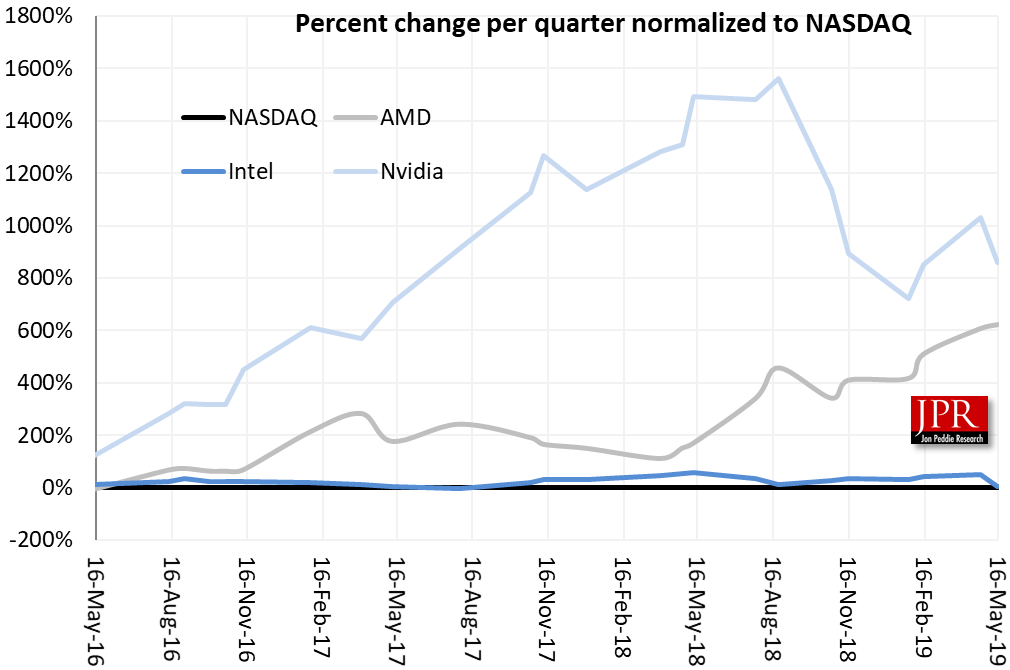

GPU includes GPU revenue in GeForce, Quadro, Tesla, and OEM. Gaming includes GeForce DT/NB, Switch, Other like GeForce Now, G-SYNC, Nvidia includes its Nintendo (Switch) business in with its gaming revenue as well. Nonetheless, the valuation placed on the company is quite high and the announcement of the acquisition of Mellanox shows Nvidia’s continued commitment to shift the company’s business from being PC and gaming dependent to being more of a data center company, a strategy also being followed by AMD and Intel.

Nvidia launch of its Turing GPU architecture, which we say is its most important innovation since the invention of the single chip GPU more than a decade ago, hasn’t had the lift some expected. The company needs to get more game developers to adopt the RTX and DLSS technology to get the gamers excited.