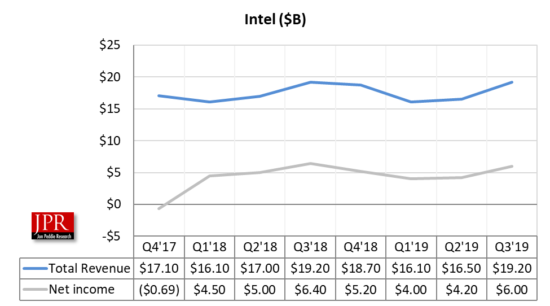

Intel revenue for the quarter was up 16.4% from last quarter to $19.2 billion, GAAP profit was $6 billion, up 43% from last quarter—7 nm queued up.

Intel beat Wall Street expectations on its third-quarter financial performance sending the company’s stock up 6.9% in morning trading Friday after the chipmaker reported late-Thursday afternoon.

Intel reported its calendar Q3 2019, revenues were flat year-over-year and grew significantly quarter-to-quarter. The PC-centric business and data-centric revenue increased over 10% and 28%, respectively, over the last quarter. Marking the best quarter for Intel in its history, Intel saw a boost from data-centric revenue.

We’ve been on a multiyear journey to reposition Intel’s portfolio to take advantage of the exponential growth of data. Our third-quarter financial performance underscores our progress as our data-centric businesses turned in their best performance ever, making up almost half our total revenue in a record quarter,” said Bob Swan, Intel CEO. “Our priorities are accelerating growth, improving our execution and deploying capital for attractive returns. We now expect to deliver a fourth record year in a row.

Client Computing Group

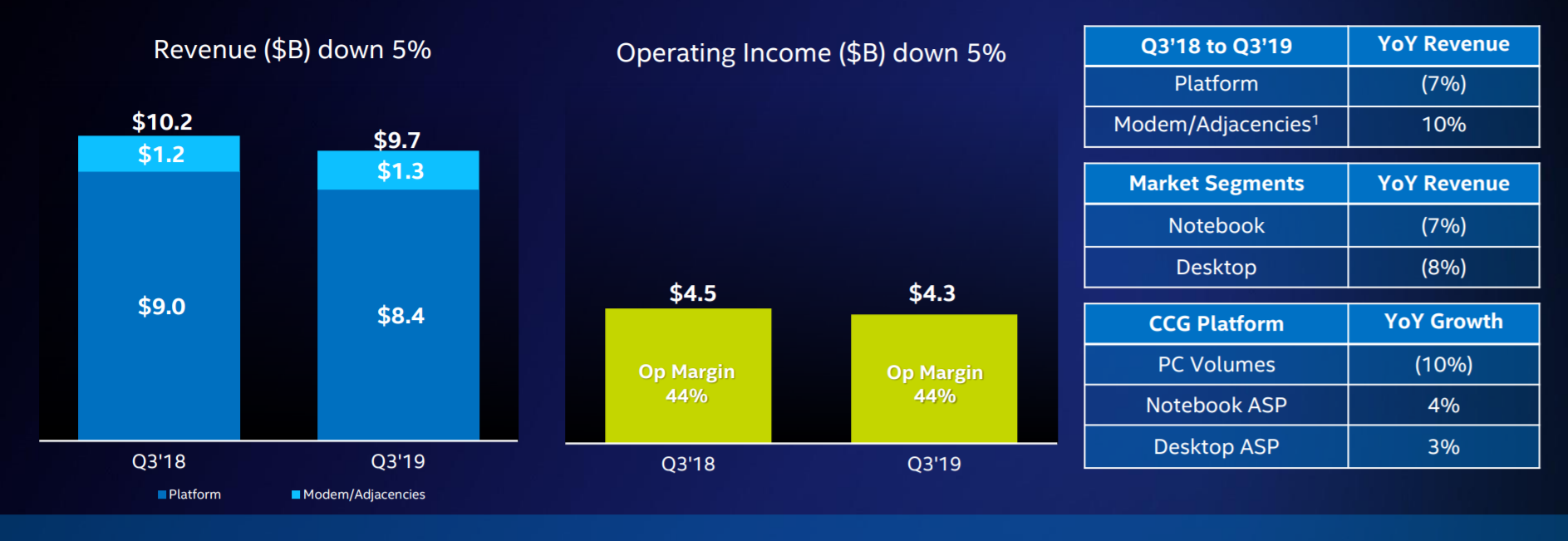

The PC-centric business (CCG) was down 5% in the third quarter on lower year-on-year platform volume, partially offset by a strong mix of Intel’s higher performance products as the commercial segment of the PC market remained strong. Major PC manufacturers introduced systems featuring the new, 10-nm-based 10th Gen Intel Core processors (code-named “Ice Lake”). Eighteen new Ice Lake-powered system designs have been shipped to date, with a total of 30 designs expected to launch in 2019. The company also announced new 10th Gen Intel Core mobile PC processors (formerly code-named “Comet Lake”) and new Intel Xeon W and X-Series processors for workstations and high-end desktops.

Revenue was down YoY due to lower platform volume, partially offset by ASP strength Operating income down on lower revenue, partially offset by lower spending.

Collectively, Intel’s data-centric businesses achieved record revenue in the third quarter, up 6% YoY. The Data Center Group (DCG) delivered record revenue driven by a strong mix of high-performance Intel Xeon processors and growth in every segment of the business. The communications service provider segment grew 11% while the cloud segment returned to growth, up 3%, and enterprise and government revenue grew 1%. The Internet of Things Group (IOTG) also achieved record revenue, up 9% on strength in retail and transportation. Mobileye achieved record revenue, up 20% YoY on increasing ADAS adoption. Intel’s memory business (NSG) also achieved record revenue, up 19% YoY. The Programmable Solutions Group (PSG) shipped the first 10-nm-based Intel Agilex FPGAs in the third quarter. PSG third-quarter revenue was up 2% YoY.

Raymond James analyst Chris Caso commented, “In particular, enterprise server grew 50% quarter over quarter—management noted they believed $200 million of Q3 revenue was China-related pull-ins, but our math suggests the impact could have been much higher, since it doesn’t make sense to us that enterprise would have accelerated in the current environment,” he said. “Looking forward, server pull-ins coupled with the potential for client inventory (driven by shortage fears) could create a headwind for 2020.” Caso rates Intel’s stock at underperform.

Spending for R&D was $3.2 billion, down -6.7% from last quarter, and down -6.4% from last year.

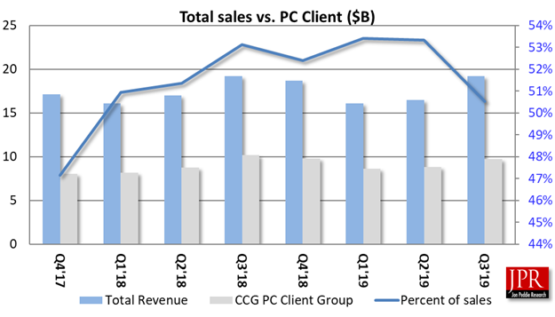

Just over half (51%) of Intel’s revenue comes from Client Computing. CCG includes platforms designed for end-user form factors, focusing on higher growth segments of 2-in-1, thin-and-light, commercial and gaming, and growing adjacencies such as WiFi and Thunderbolt.

Outlook

The company has raised its full-year revenue outlook to $71 billion, up to $500 million from April guidance. It is now expecting full-year GAAP EPS of $4.42 and raising full-year non-GAAP EPS outlook to $4.60.

What do we think?

Intel Corp. reported a surprise increase in data-center revenue en route to a big-earnings beat, but some are questioning the sustainability of the company’s momentum.

One issue in the aftermath of the report is the company’s disclosure that about $200 million of its revenue came from customers moving up their spending in anticipation of future tariffs. Several analysts wonder if that figure is telling the whole story.

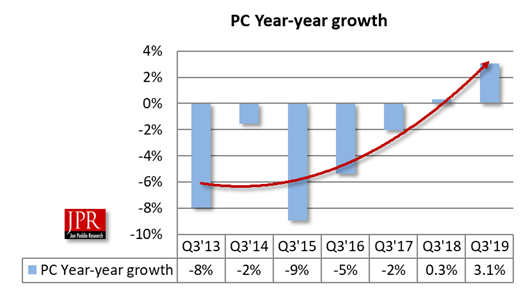

The PC trend has definitely swung up, as shown in the figure. Having PC sales go up in Q3 is not unusual for seasonality models. However, it may be warp due to pent up demand and Intel’s problems getting its 10-nm parts out in volume.

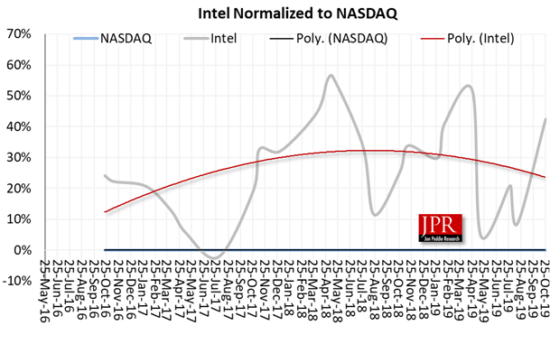

Intel’s share price has exceeded the value it was last year, and increased relative to the NASDAQ.

But remember, even though Intel bills itself as a data center company, over 50% of overall business comes from the PC, and only 30% from the data center.