Jon Peddie Research (JPR), the leading research and consulting firm for graphics and AI technologies, has released its latest quarterly report on AI processors, covering developments during the third quarter of 2025.

As of the end of the quarter, JPR has now identified 102 start-ups and 35 publicly held companies for a total of 137 companies actively manufacturing or planning to manufacture AI processors. These companies fall into two broad categories: established public companies and VC/grant-funded start-ups—what JPR calls “whales” and “start-ups,” respectively.

Investors have poured over $13.5 billion into AI-processor start-ups since 2006. Although the surge of new entrants from 2017 to 2021 has slowed, competition across the segment remains intense. JPR analysts project that, as consolidation accelerates through the decade, the number of active AI processor firms will contract sharply—mirroring the historical cycles seen in 3D graphics and XR. By 2030, they expect only about 25 specialized AI-processor companies to remain, representing a maturing market focused on efficiency, scale, and differentiated architectures.

The AI processor (AIP) market has five segments: Vehicles (which includes ambulatory robots), Edge (PCs and smartphones), AI IoT (including toys), AI Training, and AI Cloud Inference. Severing those segments, AIP suppliers offer IP only, chips, GPU, NPU, CIM, neuromorphic, RISC-V, x86, Arm CPU, analog-based, and computer vision AI processors, clearly demonstrating that one size does not, and cannot, fit all needs and applications.

The report includes:

- A comprehensive list of 137 AI processor suppliers

- Analysis of the shifting U.S.–China competitive landscape

- Profiles and interviews with notable start-ups and established players

- Trends in VC investment and market maturity

U.S. companies continue to dominate AI hardware and software, but that position faces growing pressure. Chinese firms, such as DeepSeek, are introducing competitive architectures, while U.S. regulatory policies remain inconsistent. The report indicates that this uncertainty is forcing American developers to accelerate product cycles, streamline operations, and prioritize efficiency to maintain an edge. Meanwhile, many Chinese firms that once represented potential customers have become direct rivals, intensifying the global race to deliver faster, more cost-effective AI technologies.

“This is a most exciting and opportune time for investors and established public companies to get involved with the 100-plus start-ups that have novel ideas and ambitions,” said Dr. Jon Peddie, president of JPR. “It truly is gold rush days, and not everyone is going to find that golden vine, but some of the investors and developers are going to reap enormous financial gains, as the AI boom shows no sign of abating.”

The new Q3’25 edition of the AI Processors Quarterly Update report contains all the above information and more, including a database of all the suppliers. Subscribers also receive access to direct support, custom data requests, and analyst introductions.

To learn more or to subscribe, visit www.jonpeddie.com.

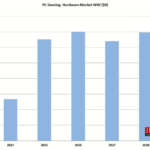

JPR also publishes a series of reports on GPU quarterly shipments, CPU shipments, the graphics add-in board market, the workstation market, and the PC gaming hardware market. The latter covers the total market, including systems and accessories, and examines 31 countries.

Pricing and availability

JPR’s Q3’25 AI Processors Quarterly Update report is available now for $4,000 for four quarterly issues, which includes a half hour of telephone consulting time per quarter, or $2,500 for a single issue with telephone time. Also, there is a bundle opportunity with the massive 357-page Annual AIP Market report.