New JPR report shows start-ups more than doubled from 2018, consolidation now ~3 deals per year.

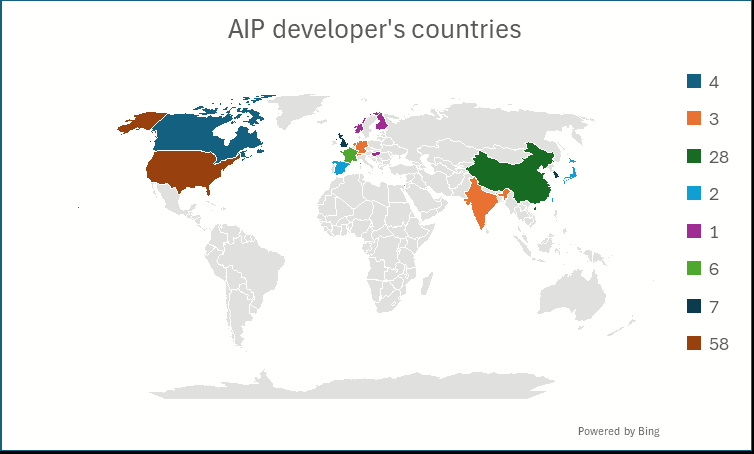

Jon Peddie Research (JPR) has published its evergreen 2025 AI Processor Report, a 357-page market map of 137 companies offering dedicated AI silicon or IP across 18 countries. The study details products, funding, leadership, geography, and SWOTs, and quantifies a $387 billion market driven mainly by inference (cloud and local) and edge deployments (wearables to PCs).

Key findings:

- Who & where: 137 AIP vendors profiled; 70% privately held; most founded within the last seven years.

- Strategy shift: Company focus is concentrated in cloud/local inference and edge; training remains capital-intensive.

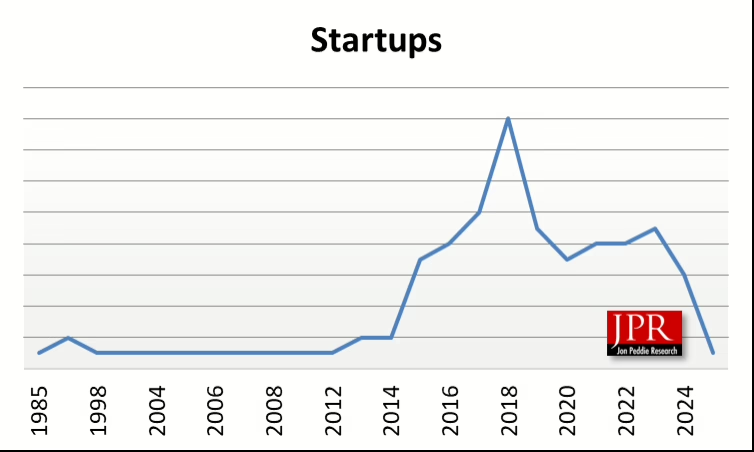

- Start-up wave has crested: The peak formation year was 2018 (by then, 54% of start-ups had already appeared).

- Consolidation baseline: Since 2022, the sector averages approximately three acquisitions per year.

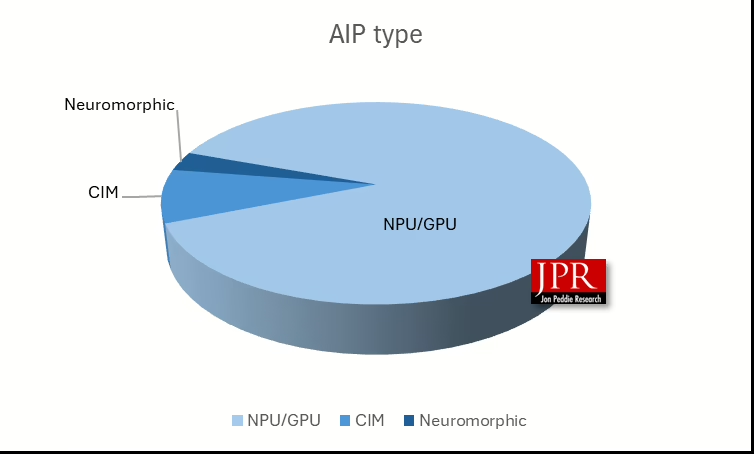

- Tech mix: Offerings span GPUs, NPUs, CIM/PIM, neuromorphic processors, and matrix/tensor engines. (CPUs and FPGAs are excluded from market totals due to functional generality.)

- Inside an AIP: Common patterns include tensor/matrix engines, near-compute SRAM + HBM/DDR, NoC fabric, and PCIe/CXL/NVLink/Ethernet off-chip links.

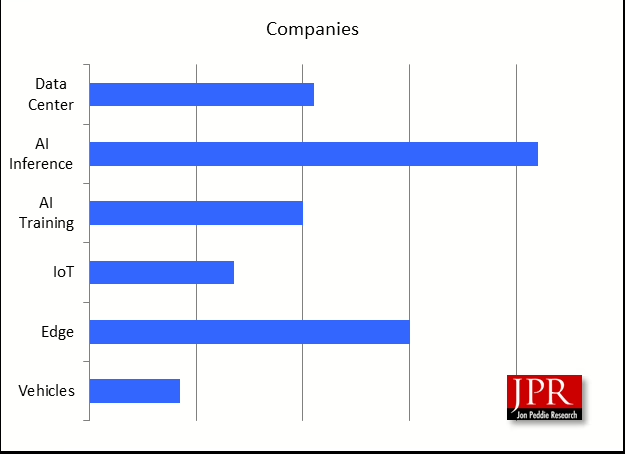

Market segmentations and taxonomy

The combination of LLM inference at scale, edge AI proliferation, and memory-bound workloads is reshaping silicon roadmaps. JPR’s taxonomy clarifies who is building what, where capital is flowing, and which designs align with near-term demand.

An AI processor (AIP) is a chip optimized to run neural network workloads fast and efficiently by doing huge amounts of tensor math while moving data as little as possible.

Of the five major market segments, Inference (cloud and local) and Edge (wearables to PCs) are the areas where the companies are putting most of their efforts.

Of the privately held companies, has the window closed? The peak in start-ups happened in 2018, five years before Nvidia’s sales exploded. And by then, 54% of the start-ups appeared.

Since 2022, there has been an average of three acquisitions every year.

AIPs are being offered as GPUs, NPUs, CIMs, Neuromorphic processors, CPUs, and even FPGAs. Our report does not include CPUs and FPGAs in its evaluation of the market because their generality makes them impossible to differentiate by function.

What an AIP looks like inside

- Compute blocks: wide SIMD/SIMT cores (GPU style), tensor/matrix engines (systolic arrays), vector units, activation units.

- Memory hierarchy: small, fast SRAM near compute; larger HBM/DDR off-chip; caches or scratchpads; prefetchers/DMA.

- Interconnects: on-chip NoC; off-chip links (PCIe/CXL/NVLink/Ethernet).

- Control: command processors, schedulers, and microcode for kernels/collectives.

Methodology

The AIP report is an annual evergreen report augmented by quarterly updates. We continuously monitor the companies’ development and interview their management. The report comes with a copy of our in-depth database on the companies, which we update weekly. Subscribers can contact us for the latest updates. JPR also has an RAG LLM, which concierge clients can access for customized reports and the creation of presentations.

More information about the Annual AI Processors Market Development report can be found here. It can be purchased for $6,000. There is also a bundle option that includes this annual report along with JPR’s AI Processors Quarterly Update report series for $8,000.

JPR also publishes a quarterly report on unit shipments of GPUs, workstations, graphics boards, and RISC-V processors.

==============

What’s not in the report?

We have not included FPGA suppliers (e.g., Achronix, AMD’s Xilinx Versal, Efinix’s Trion/Titanium, Gowin Semiconductor, Microchip Technology, and others).

We also excluded computer vision AI processor suppliers—e.g., Ambarella, Axera (China), Blaize, BrainChip (Akida), Ceva, Eta Compute, Flex Logix, GreenWaves Technologies, Gyrfalcon Technology (GTC), Himax (WiseEye AI), Perceive, Quadric, Recogni, Reneasa, and others—and may include them in an appendix in a future edition.