AMD revenue was flat, and Intel was down. The overall market was down 2.9% sequentially.

Graphics chips and boards sales in the first quarter of 2013 were not robust. Of the three top vendors, only Nvidia sales were up quarter to quarter, AMD and Intel were down. The report comes from market research supplied by Jon Peddie Research, the industry’s research and consulting firm for graphics and multimedia.

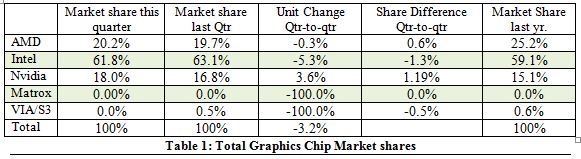

AMD lost 0.3%, quarter-to-quarter, Intel slipped 5.3%, and Nvidia increased by 3.6%. The overall PC market declined 13.7% quarter-to-quarter while the graphics market only declined 3.2%, reflecting an interest on the part of consumers for double-attach, the adding of a discrete GPU to a system with integrated processor graphics.

On a year-to-year basis JPR found total graphics shipments during Q1’13 dropped 12.9%; PCs shipments declined by 12.6% overall. GPUs are traditionally a leading indicator of the market, since a GPU goes into every system before it is shipped. Most PC vendors are guiding down to flat for Q2’13.

The popularity of tablets and the persistent economic malaise are the most often mentioned reasons for the altered nature of the PC market. Nonetheless, the compound annual growth rate (CAGR) for PC graphics from 2012 to 2016 is still 2.6%. JPR expect the total shipments of graphics chips in 2016 to be 394 million units.

The ten-year average change for graphics shipments for quarter-to-quarter is a growth of -2.2%. This quarter is below the average with a 3.2% decrease.

JPR findings include discrete and integrated graphics (CPU and chipset) for Desktops, Notebooks (and Netbooks), and PC-based commercial (i.e., POS) and industrial/scientific and embedded. This report does not include handhelds (i.e., mobile phones), x86 Servers or ARM-based Tablets (i.e. iPad and Android-based Tablets), Smartbooks, or ARM-based Servers. It does include x86-based tablets.

The quarter in general

- AMD’s quarter-to-quarter total shipments of desktop heterogeneous GPU/CPUs, i.e., APUs jumped 30% from Q4 and declined 7.3% in notebooks. The company’s overall PC graphics shipments slipped 0.3%.

- Intel’s quarter-to-quarter desktop processor-graphics EPG shipments decreased from last quarter by 3%, and Notebooks fell by 6.3%. The company’s overall PC graphics shipments dropped 5.3%.

- Nvidia’s quarter-to-quarter desktop discrete shipments were flat from last quarter; and, the company’s mobile discrete shipments increased 7.6%. The company’s overall PC graphics shipments increase 3.6%.

- Year-to-year this quarter AMD shipments declined 29.4%, Intel dropped 8.8%, Nvidia increased 3.6%, and VIA fell 8.4% from last year.

- Total discrete GPUs (desktop and notebook) were up 1.1% from the last quarter and were down 11% from last year for the same quarter due to the same problems plaguing the overall PC industry. Overall the trend for discrete GPUs is up with a CAGR to 2016 of 2.6%.

- Ninety nine percent of Intel’s non-server processors have graphics, and over 67% of AMD’s non-server processors contain integrated graphics; AMD still ships IGPs.

Year to year for the quarter the graphics market decreased. Shipments were down 15.8 million units from this quarter last year.

Graphics chips (GPUs) and chips with graphics (IGPs, APUs, and EPGs) are a leading indicator for the PC market. At least one and often two GPUs are present in every PC shipped. It can take the form of a discrete chip, a GPU integrated in the chipset or embedded in the CPU. The average has grown from 1.2 GPUs per PC in 2001 to almost 1.4 GPUs per PC.

Report availability

The Q1’13 edition of Jon Peddie Research’s Market Watch is available now in both electronic and hard copy editions, and sells for $2,500. Included with this report is an Excel workbook with the data used to create the charts, the charts themselves, and supplemental information. The annual subscription price for JPR’s Market Watch is $4,000 and includes four quarterly issues. Full subscribers to JPR services receive Tech Watch (the company’s bi-weekly report) and a copy of Market Watch as part of their subscription. For information about purchasing Market Watch, please call 415/435-9368 or visit the Jon Peddie Research website at www.jonpeddie.com.